Author:

Tom Matterson

Investment Manager,

Saltus Asset Management Team

Reviewed by: David Cooke, Co-Chief Investment Officer , Saltus Asset Management Team

As we approach the midpoint of 2025, the geopolitical, economic and financial market landscape has undergone seismic shifts, with potentially far-reaching implications for investors. In this article, we focus on some of these changes and suggest how investors can chart a course through these shifts.

The Three ‘T’s

Trump, tariffs, turmoil. If we only had three words to sum up the first five months of 2025, these would do a pretty good job. Trump’s whirlwind of tariff announcements since his inauguration in January have been an almost constant feature on newsreels. Since ‘Liberation Day’ on 2nd April, when Trump stunned the world from the quaint setting of the White House Rose Garden, the average global tariff rate has been in a state of flux.

Rather than list all the tariff announcements thus far (which would instantly go out of date anyway), what we can say with confidence is that the average global tariff rate is, and will continue to be, higher than it was at the start of 2025. Tariffs are essentially a tax on consumption, and so the expectation is that consumption will slow as a result, supply chains will gum up, trade activity will slow, and eventually the economy will too. These are the first order effects.

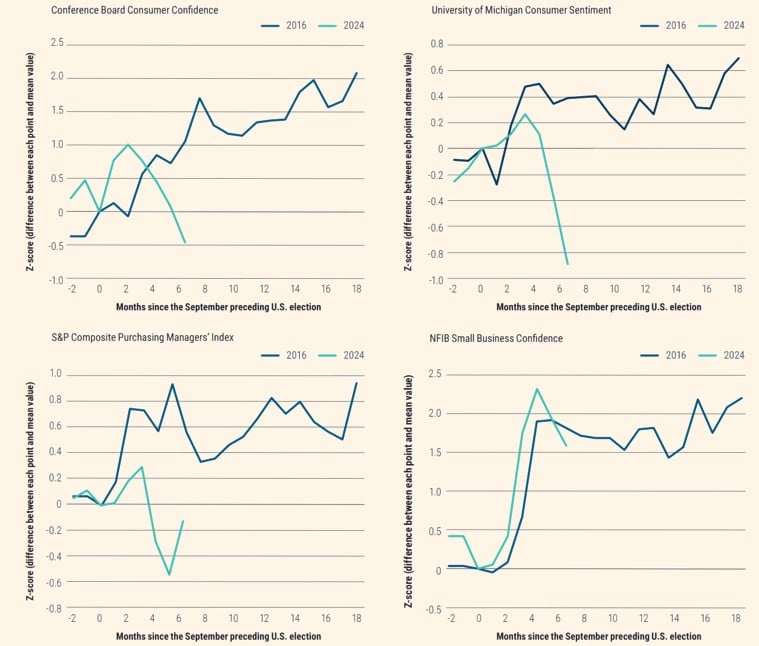

The second order effects stem from the uncertainty that these sporadic and disjointed announcements cause. We are hearing from more and more businesses that they are putting off hiring and investment decisions as it is impossible to make long term business forecasts in this environment. US business and consumer sentiment surveys have fallen off a cliff [1]. Even if some or all of the announced tariffs were rolled back, it is likely the uncertainty has already done enough damage to sentiment, and unless businesses indicate they will start investing again, and the economic data holds up, it is likely there will be a slowdown in the months to come.

US sentiment surveys have deteriorated

Source: Conference Board, University of Michigan, S&P, NFIB, Haver Analytics and PIMCO as of 31 March 2025

Stock markets have taken this in their stride though. If you had looked at the US market at the end of March, and not again until the end of April, you would have seen a negligible 0.7% decline – nothing to see here. This masked a huge amount of volatility in the month. For example, in the Liberation Day aftermath the S&P500 fell 11% over the next two days. Only Covid, the collapse of Lehman Brothers, and Black Monday in 1987 have caused worse two-day falls [2]. Despite this, we then had an extraordinary turnaround on 9th April, when the index posted its best day since World War II, rallying 9.5% when Trump announced a pause in his reciprocal tariff agenda. The market took another wobble though when Trump started talking about firing the Chairman of the Federal Reserve, the most important job in finance. However, he quickly reversed course on this once he saw the market’s reaction, perhaps after a quiet word from his seemingly rational Treasury Secretary – Scott Bessent. Stock markets have continued their recovery and indeed wiped out all losses since the start of 2025, given resilient economic data, and a steady stream of tariff deals starting to be released from the White House.

The Decline of the dollar

The moves elsewhere in US markets have been more interesting. US treasury bonds and the US dollar are typically shelters in market storms, as investors seek safety in these assets, and in recent years there has been a strong relationship between the two. However, in April when US stocks were in free fall after Liberation Day, this relationship broke down and both US bonds and US dollars fell too, a dynamic more akin to emerging markets (and the UK) [3]. This was a US-focused shock, so investors scrambled to shed their US assets. These events are forcing investors to question the ‘US exceptionalism’ trade that investors have enjoyed for so long.

The dollar’s relationship with US yields has broken down

Source: Financial Times, LSEG, @raydougles.bsky.social

Even as US stocks have recovered, the dollar has continued to fall. The US Dollar Index (DXY) has fallen over 8% in the year to the end of May. Even after these moves, the index still trades significantly above its average since the start of the floating exchange rate era in 1973 [4]. Much of the dollar’s strength can be attributed to its status as the world’s reserve currency, as over half of international trade is priced and invoiced in dollars, and nearly 60% of the world’s international reserve holdings are in dollars despite US GDP only comprising about a quarter of world income [5].

Given the lack of any credible alternatives, it is likely that the dollar will continue to be the world’s dominant currency. What could change though, is that countries could start moving their reserves out of US dollars, and foreign investors could sell their US assets. We have seen evidence of both these things in the last few months, and the dollar has declined accordingly.

Who will fund the US?

Much of the fuel for Trump’s anger at the global trading system is the fact that the US runs a large trade deficit with the rest of the world, given it imports more goods than it exports. This has resulted in a multi-decade decline in US manufacturing activity. On the flip side, as US consumers have spent their dollars around the world, countries have recycled these dollars into US assets, be these US government bonds, or the Magnificent Seven group of technology stocks. Estimates of foreign holdings of US assets range from $20-30tn [6]. These capital flows into US assets have funded a profligate US government, and the ‘US exceptionalism’ trade which has propelled US assets against all-comers for a number of years now.

Total foreign holdings of US equities, Treasuries and US Credit

Source: Apollo, Federal Reserve, MacroBond

If Trump does succeed in reducing the US trade deficit, or global trade slows down, then there will be fewer dollars in circulation to be recycled into US assets. Thus, a key support for US assets could fall away. Either the demand has to be taken up by US investors, or prices will have to fall. Additionally, as questions start to be asked about the reliability of the US administration, the credibility of US institutions, the US government’s substantial debt pile, and the attractiveness of US capital markets, foreign investors could start selling down their holdings of US assets.

Both of these factors could significantly damage the US financial sector’s ability to fund future US growth, so serious considerations must now be given to a portfolio’s US asset exposure.

Europe gets fiscal

Turning away from the US now, Europe is also undergoing substantial shifts from a policy standpoint. For two decades now, Europe has lagged behind its developed market peers, and investors have shunned the region given weak demand and slow productivity growth. This could be beginning to change, and indeed European stock markets have been some of the best performing in the first five months of 2025.

In February the US Vice President – JD Vance – gave a fiery speech at the Munich Security Conference where he took aim at European leaders for censorship and the suppression of free speech. Vance said the biggest security threat facing Europe was not Russia or China, but the ‘threat from within’ [7]. The speech was preceded by Trump questioning the future of NATO, and snubbing Ukraine and Europe’s leaders by offering a generous peace deal to Putin without speaking to them first.

The message was clear; the US was not going to support Europe militarily to the same extent going forward.

Shortly after these events, in mid-March, three momentous European policy announcements were made in quick succession.

- The European Union unveiled the ReArm Europe Plan – an initiative to enable €800bn of spending to boost Europe’s defence capabilities [8].

- The German Schuldenbremse (the so-called ‘debt brake’) was reformed – allowing defence spending to increase without constraint [9].

- The new German government announced a €500bn infrastructure fund.

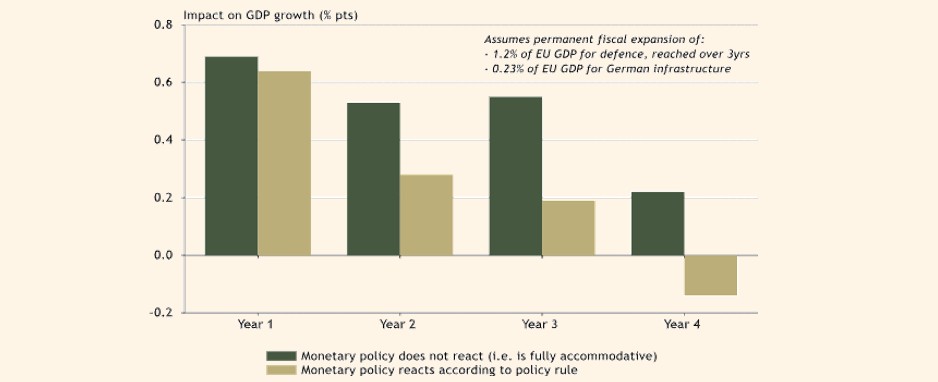

This additional spending could result in structurally higher growth in Europe given the potential for higher productivity. It is estimated that we’ll see EU GDP growth above 2% over the next 3 years [10], significantly above recent trends. However, it will take time for spending to ramp higher, so in the short term Europe may be negatively impacted by a global economic slowdown as a result of tariffs, before the positives kick in.

Fiscal expansion to bolster European growth

Source: Absolute Strategy Research Limited, LSEG, ECB

Although most of the focus is on tariffs for now, Trumpism may have resulted in a significant and long-lasting boost to the continent by addressing weak demand, and developing badly needed capabilities in areas like infrastructure, defence, industrial capacity and governance.

A more positive European backdrop, combined with a more negative US backdrop over the medium term could result in a reallocation of capital back east across the Atlantic, and we may just be at the start of a period of European outperformance.

All that glitters

Gold has continued its strong run in 2025, continuing to make new highs. Gold demand has been given a boost by the uncertainty we’ve been seeing, but after such a good period investors are now starting to ask themselves how much further it has to run.

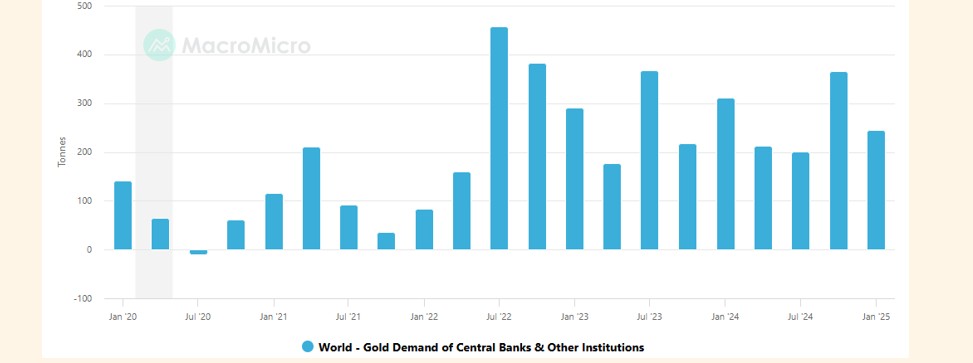

Since the US weaponised the US dollar in 2022 by freezing Russia out of the dollar trading system following its invasion of Ukraine, countries have been reassessing their US dollar exposure in case this ever happened to them. Data shows that central banks have been large buyers of gold over the last couple of years [11][12], as they convert US dollar reserves to gold. This has provided a healthy tailwind for the yellow metal.

Central Bank gold net purchases

Source: World Gold Council, MacroMicro

More recently, gold has been perhaps the best beneficiary of high levels of uncertainty and market volatility driven by US policy and a flight from US assets. Although we may have reached ‘peak uncertainty’ in early April, what we have learnt since is that policy uncertainty and market volatility are going to be constant features of this Trump government. As such, gold is likely to continue to act as a safe haven asset especially with US treasuries and US dollars losing their protective status.

There are short term factors at play too. Speculative positioning is below its long term average, and there are signs that Asian retail investors have been active in the gold-backed ETF market, possibly given the low yields on Chinese government bonds. These point to the price gains still having room to run [13].

Our portfolios

There are of course many other areas of interest and concern as we move into the second half of 2025, and we will write more about these in the coming weeks.

- Will absurd US-China tariff levels and a pause in trade result in China having to wheel out the ‘fiscal bazooka’ that we became accustomed to in the 2010s? (unlikely)

- Has the UK market turned a corner after its strong start to 2025? (possibly)

- Are emerging markets beneficiaries of trade tensions through more trade with China and a weaker dollar, or are they in Trump’s crosshairs given they export more to the US than they import? (more the former)

- How concerned should we be about the rise in yields of long-dated Japanese bonds? (potentially very)

At Saltus Asset Management, we are constantly assessing these factors and positioning portfolios to reflect our views. Our latest Asset Allocation Update can be found here Asset allocation update April 2025 : How we’re thinking about markets… | Saltus.

At a high level, our recent asset allocation decisions have been taken with a view to increasing portfolio diversification across all risk bands. Building truly diversified portfolios to maximise risk-adjusted returns is at the core of our investment approach. We think this has become especially pertinent in an increasingly unsettled world.

At a broad asset class level, we have gradually been reducing overall equity exposure over the last six months. Equities had a positive run in 2023 and 2024, and a noisier outlook for markets in 2025 meant we wanted to book some profits and invest the proceeds in alternative asset classes to increase the portfolios’ diversification and resilience in more volatile markets.

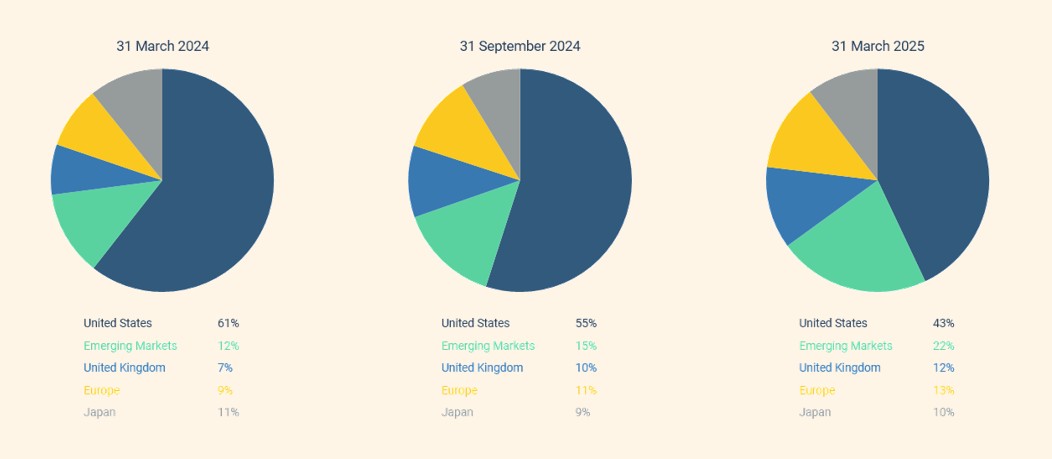

Within our equity book, in the autumn of 2024 we began gradually reducing US equity exposure as the political situation was becoming murkier the closer we got to the presidential election. US equities had travelled a long way and were priced for a perfect scenario continuing, which was hard to match up with an increasing likelihood of a Trump victory and the trade rhetoric that came with it. We used the proceeds to bolster our equity positions in Emerging Markets, Europe and Japan, thus spreading our equity risk geographically, reducing our dependence on the US stock market, and reducing our US dollar exposure in the process. These moves shielded portfolios from the worst hit markets in March and April. We continue to move in this direction given the points touched upon in this article.

Geographic equity allocation over time

Source: Saltus

In our alternatives asset allocation, we continue to hold our gold positions, be those physical gold positions in lower risk portfolios, or gold miners in higher risk portfolios. We think there is still room for the gold price to run given some of the reasons mentioned above, and gold plays a useful role of hedging against more uncertainty and volatility from here. We have sold out of our copper position over concerns about the path of global economic growth, especially in China. We are still positive on the long term story for copper given structural demand growth and limited supply, but we think there will be a more attractive entry point. We have been bolstering our allocation to global macro hedge funds and long/short funds as we believe our exposure in these areas can benefit from more volatile financial markets, and provide portfolio ballast if the equity and bond allocations are suffering.

Over the last five years we have seen significant shifts in the investing environment. Covid, war, double digit inflation, rising interest rates, and a reconfiguration of the global trade and security system, to name a few. Together, these shifts represent a meaningful departure from the investment environment that we’ve enjoyed over the last twenty years. We should therefore not expect yesterday’s winners to continue winning and must keep an open mind when trying to predict tomorrow’s winners. From where we stand today, it is hard to forecast the long term impacts of these shifts, but a core belief in portfolio diversification and keeping a long term view should help investors navigate this changing landscape.

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.