In your mid-40s with £250,000 in your pension pot? Wondering if you really need to wait until 67 to retire? Perhaps not. With some thoughtful planning and investing, early retirement could be within reach.

Here we will explore the pros and cons, the financial strategies to consider, and what it might take to make a £250,000 pension support an early retirement.

Determining your retirement expenses and setting realistic goals

So, what is a comfortable retirement? Pensions UK and the University of Loughborough have researched the amount required per annum to provide a ‘comfortable retirement.’ They concluded that, for an individual, it was around £45,400 a year. This sum certainly isn’t a lavish figure: it’s enough to provide around £78 a week on groceries, enjoy around two weeks of holiday in Europe, and spend around £1,500 a year on clothes and shoes.[1]

How much you need in retirement is highly individual and depends on your expectations. Think about the lifestyle you want, how much you plan to travel, your hobbies, and whether you’d like to support family members. A useful starting point is reviewing your current annual expenses, recognising that some costs may decrease (such as commuting), others may stay broadly the same, and certain expenses, particularly healthcare, are likely to rise, especially in later years of retirement.

Understanding what a £250k pension pot means

You can begin accessing your pensions from age 55 (rising to 57 in 2028).[2] The most common and flexible way to access your pension is through income drawdown, where your pot remains invested, and you withdraw income as needed. This approach can allow for continued growth potential, tailored withdrawal strategies, and adaptability as your needs change.

So, how much will a pension pot of £250k pay out as an income? That depends on factors such as how you choose to access it and how long you need it to last.

Realistically, if you were wanting to retire with a £250,000 pension pot at 55 with no other income sources or assets, it would be incredibly difficult. However, if you had other income sources or retired a little later, it could be possible. Assuming a withdrawal rate of 3-4% you could expect to withdraw around £7,500 to £10,000 gross a year solely from your retirement pot. A long way off a ‘comfortable retirement’, especially if you plan to retire early and have a number of years before you can access the State Pension.

Having long term success in retirement can depend on how well you manage the following factors:

- Withdrawal rate

Getting your withdrawal rate right can be tricky but it’s important. Ultimately, your withdrawal rate can impact how long your pension pot lasts.

Factors like your spending needs, other income sources, property wealth, and investment mix all play a role in shaping the right approach. A financial adviser can help tailor a withdrawal strategy that suits your lifestyle and long term goals.

- Investment performance

When using drawdown, your pension remains invested, which can offer continued growth but can also introduce market risk.

Poor performance in the early years of retirement (known as sequence of returns risk) may reduce your pot’s longevity. This is because withdrawing money during market downturns can lock in losses, leaving less invested to benefit from future market recoveries. Professional management and diversification may help mitigate this.

- Taxation

Typically, 25% of your pension can be taken tax free up to a limit of £268,275, with the remainder taxed as income.[3] Strategic withdrawals, particularly when coordinated with other income sources like rental income or dividends, can help minimise your overall tax liability.

- Inflation

Inflation can erode purchasing power over time. This is especially true for costs such as healthcare, travel and housing. Investments should be structured to grow in real (inflation-adjusted) terms wherever possible.

Want to retire early? Consider these saving strategies

How can you easily save for a more comfortable, early retirement? If your starting point is £250,000 in your pension at 45, to achieve this, you’ll need to save and invest around £1,500 a month until you’re 60. If you are earning £80,000, that’s roughly 22% of your annual salary. Of course, the majority of that could be made up by employer pension contributions, meaning a good chunk of it may not have to come out of your pocket. If you’re 45 today and your pot and monthly contributions are invested well, making a reasonably conservative 4% a year, by the time you arrive at your 60th birthday, you’ll have around £800,000.

The 4% Rule: A helpful tool for early retirees

William Bengen is an economist famous for creating the 4% rule after analysing 50 years of historical returns across every asset class. He determined that in all circumstances, regardless of when someone retired over the 50 years, they could take annual withdrawals of 4%, and the pot would always last 30 years.[4] By applying this rule, you could take £32,000 a year from your £800,000 retirement pot. Not quite a comfortable retirement but getting there. However, you’ve probably done some quick sums – if it did run out in 30 years and you retired on your 60th birthday, your 90th birthday could be a pretty miserable one…

There are some flaws in Bengen’s approach though and it really should just be taken as a rough rule of thumb rather than Gospel.[5] A financial adviser can provide a more detailed and tailored financial plan that takes into account your personal circumstances.

The importance of the State Pension in early retirement

Fortunately, if you’ve made around 35 years of National Insurance contributions or credits, you should be eligible for a full state pension of just over £12,500 p.a.[6] If you retire before State Pension age, you’ll have to draw entirely from your own assets until the state pension can be accessed. Thus, once you reach retirement age the state pension can be a positive boost to your retirement income. Due to the additional £12,500 of income (increasing with either inflation, average earnings or 2.5%, whichever is highest), depending on when you retire your pot could now last well into your late 90s, and you can close in on that comfortable retirement figure of £45,400 per annum.

Maximising the value of a £250k pension pot

Investing your money across different tax wrappers, to reduce the tax you’ll pay in retirement, is paramount as the £45,400 is very much a net figure. The investment strategy you employ will also be of equal importance to ensure your pot is growing at a sufficient rate to reach your early retirement objective. Two areas that are likely most effectively overseen by professionals.

Inflation is often the silent threat to long term financial plans. What seems like enough today may be less than what you need in the future. Holding too much in cash or low growth assets can erode your spending power over time, so the right allocation to growth investments is often needed to maintain your desired lifestyle. At the same time, investment decisions shouldn’t be static. Annual reviews are essential. Markets shift, tax rules change, and your personal spending needs may evolve, so revisiting your plan ensures both your withdrawals and investment mix remain aligned with your goals and the economic environment.

£250k pension pot calculator

The 4% rule or a pension calculator can be helpful tools for getting a rough idea of whether you’re on track to afford the retirement you want. While only a guide, a pension calculator lets you model different scenarios and assess how your current savings and contributions may shape your future. The Saltus pension calculator goes a step further by offering personalised projections alongside insights from our Wealth Index, based on twice-yearly surveys of over 2,000 individuals with £250,000 or more in investable assets.[7] This allows you to see how your retirement plans compare with those of others in a similar age group and financial position, including average pension pot sizes and contribution levels.

Build a retirement income plan

While useful, rather than rely solely on the 4% rule or a pension calculator, many people may benefit from working with an adviser to create a customised cash flow plan. The plan can account for various factors that will more closely reflect real life such as variable withdrawals, capital expenditures, and the flexibility to accommodate different market returns. You can also stress test some of the plan’s assumptions, which helps ensure a more comprehensive and reliable assessment of what you will personally need for retirement. Of course, even this is based on assumptions so updating the cashflow on an annual basis, and as life changes, is equally as important as creating your initial plan.[8]

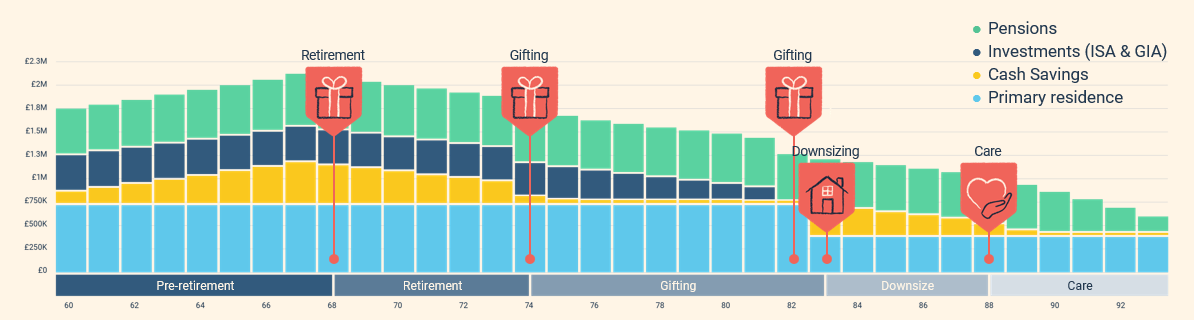

An example cashflow plan can be found below:

The Financial Conduct Authority does not regulate cash flow planning, tax advice, wills

Key questions to ask before retiring

There’s more to retirement than just how much you have in your pension pot. A sustainable retirement plan needs to account for market risks, inflation, timing decisions, and the security of your loved ones. Here are some key questions to ask yourself before you take that next step:

- When should you take your State Pension?

There is no perfect time to take your State Pension, it all depends on your personal circumstances. If you are able, deferring your state pension can increase your payments by around 5.8% for each year you wait.[9] If you aren’t able to defer your State Pension, then you can begin claiming it as soon as you reach State Pension age. State Pension age is currently 66 but rising to 67 between April 2026 and 2028, and to 68 between April 2044 and 2046.[10]

- What can you do to protect your spouse or beneficiaries?

To best protect your spouse and beneficiaries, it’s important to have up to date wills and nominate beneficiaries for your pensions and life insurance policies. Once again, clear planning and regular reviews can help ensure your loved ones are financially supported and your wishes are carried out correctly.

- How long will your money need to last?

Unfortunately, it’s impossible to predict exactly how long your retirement income will need to last, but it’s wise to plan for a longer retirement rather than risk running out of money too soon. Today, a 60 year old man in the UK has an average life expectancy of 84, with a 1 in 4 chance of reaching 92 and a 1 in 10 chance of living to 96. For a 60 year old woman, the average life expectancy is 87, with a 1 in 4 chance of living to 95 and a 1 in 10 chance of reaching 99.[11] The younger you are now, the higher your potential lifespan could be. Given this, you could be facing a retirement that lasts 30 to 40 years or more. To understand whether your pension will last, it’s essential to consider both your intended retirement age and your life expectancy.

Common mistakes to avoid

Without a clear retirement plan, it can be easy to make choices that may create challenges later. As always, professional guidance can help you avoid these pitfalls, but here are some of the more common mistakes to be aware of:

- Taking too much too soon: Withdrawing large sums early in retirement may reduce the longevity of your savings and increase the risk of running out of money sooner than expected.

- Ignoring inflation in planning: Rising prices erode the value of savings over time. Failing to factor in inflation means your retirement income may not stretch as far in the future as it does today.

- Not co-ordinating pension withdrawals with other income: If pension withdrawals are not managed alongside income from other sources (such as ISAs, property, or other investment vehicles), you could end up paying unnecessary tax or depleting tax efficient accounts too quickly.

- Overlooking spousal benefits: Some pensions and investments have features that can support a spouse or partner after your death. Not planning around this could leave your partner with less financial security than intended.

Is £250k enough to retire?

On its own, a £250,000 pension pot is unlikely to fund a comfortable or early retirement. However, with additional savings, other income streams, and a well-structured withdrawal plan, it can be a strong starting point. So, if you’re in your 40s and have £250,000 in your pension pot and want to retire early, get planning, get investing, and maybe take some advice!

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.