Author:

Jordan Gillies

Head of Business Development and Marketing,

Saltus Asset Management Team

Reviewed by: Megan Jenkins, Chartered Financial Planner, Saltus Asset Management Team

Inheritance tax (IHT) is affecting more families each year, and for many it is becoming an increasingly important part of estate planning conversations.[1] With inheritance tax thresholds frozen until at least the 2030 to 2031 tax year, and pensions set to be brought into the inheritance tax net from April 2027, estates that once sat comfortably below the limits are now being exposed to potential tax charges.

As a result, understanding the options available to reduce an inheritance tax bill is more relevant than ever. Gifting is a well-known approach, but one particularly valuable exemption can sometimes be overlooked. Known as the normal expenditure out of income exemption, or more commonly gifting out of surplus income, this relief can offer a practical and tax‑efficient way to pass wealth to loved ones during your lifetime, provided the rules are followed and the right evidence is kept.

Inheritance tax

Inheritance tax is charged at 40% on the value of an estate above certain tax‑free thresholds when someone dies. Everyone has a standard nil‑rate band of £325,000, which can be passed on without inheritance tax and is currently frozen until the end of the 2030 to 2031 tax year. In addition, there is the residence nil‑rate band, which can be worth up to £175,000 where a main home is left to direct descendants such as children or grandchildren. This means that, in many cases, up to £500,000 can be passed on free of inheritance tax.[2]

For married couples and civil partners, the position can be even more favourable. Any unused portion of the nil‑rate band and residence nil‑rate band can be transferred to a surviving spouse or civil partner. In practice, this can allow a couple to pass on up to £1 million before IHT becomes payable. However, it is important to be aware that the residence nil‑rate band is gradually tapered for estates valued at more than £2 million, which can reduce the relief available.

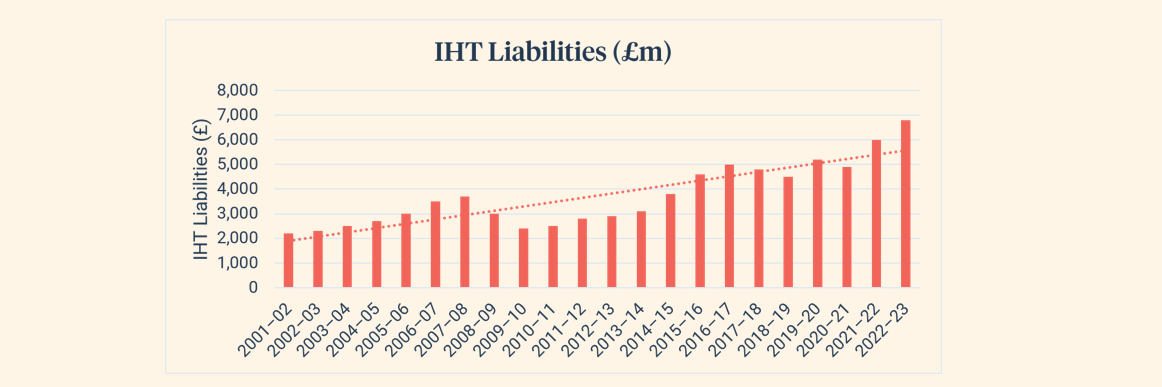

As a result of frozen thresholds and rising asset values, estates affected by inheritance tax have been steadily increasing, as shown in the graph below. With inheritance tax allowances fixed until 2030 to 2031, there is little to suggest this trend will reverse anytime soon. Research from the London School of Economics reinforces this picture, forecasting that inheritance tax revenues will double in real terms by the 2032 to 2033 tax year.[3]

Source: Gov UK[4]

2027 pension reforms

In addition, from April 2027, the way pensions are treated for inheritance tax purposes is expected to change. Proposals announced in the 2024 Autumn Budget would bring unused defined contribution pension funds within the scope of inheritance tax for the first time. For those who have historically used pensions as a tax‑efficient way to pass on wealth, this represents a meaningful shift in estate planning.

Under the current rules, pensions typically sit outside an individual’s estate for inheritance tax. From 2027, however, any unused pension funds at death are expected to be included in the value of the estate and may be subject to inheritance tax, depending on the allowances available.[5] These changes underline the importance of reviewing how pensions fit within your wider estate planning strategy and considering other ways to manage IHT, including gifting during your lifetime.

Gifting out of surplus income

Gifts out of surplus income can be a valuable inheritance tax exemption, but HMRC applies some clear conditions. To qualify, the gifts must be made regularly and form part of a normal pattern of spending, rather than something done on a whim. This usually means there is a history of gifts over a number of years. HMRC often looks for a track record of three or four years, but that is not a hard rule. A shorter period can still work if it is clear from the outset that the intention was always to make ongoing gifts. The gifts will also typically be of a similar size to one another, helping demonstrate a regular pattern of gifting.[6]

This is where good planning can make a real difference. If you have a documented plan showing that you intend to make regular gifts, either indefinitely or over a number of years, that evidence can carry real weight. Setting up a standing order, committing to pay regular costs such as insurance premiums, or clearly recording the intention to gift surplus income as part of a wider financial plan all help demonstrate that this is a deliberate, long term strategy.

In some cases, that can mean even a single gift could be argued to fall outside the estate, as long as it sits within a clearly defined pattern rather than being a one-off. It’s a great example of why having a written financial plan and working with a financial adviser is not simply a box-ticking exercise but something that can have a very real impact.

The gifts themselves are usually made in cash and do not have to be made at fixed intervals or to the same recipient, provided there is a recognisable pattern over time. Importantly, the gifts must be made out of income, not capital. Income for this purpose is net income after tax and typically includes earnings, pension income, interest, dividends and rental income. Pension drawdown withdrawals can count as income, including any tax-free element, if they are taken regularly in a way that looks like ongoing income rather than a one-off extraction of capital. Income that has been reinvested or left untouched for a long period, such as in an ISA, is usually treated as capital and may not qualify.

Finally, the gifts must come from surplus income, meaning income left over after meeting normal living expenses. Making the gifts should not reduce the donor’s usual standard of living. Everyday household costs, regular leisure spending and lifestyle expenses are taken into account when assessing this. If capital has to be used to maintain day-to-day living, this is a strong sign that there is no true surplus, and the exemption may be restricted or lost.

What doesn’t count as income?

There are some clear exemptions for what doesn’t count as income and therefore cannot be used for gifting out of surplus income. These include:

- Capital or returns of capital

- The capital element of purchased life annuity payments (only the interest element counts as income)

- Bond withdrawals, even where a chargeable event gain arises

- Payments from discounted gift trusts or loan trusts

- Income that has been reinvested or accumulated (e.g. accumulation units)

- Income left unused for extended periods (typically over two years), which HMRC may treat as capital

- Income transferred from one spouse or civil partner to another, as each individual’s income is assessed separately

How to claim

You don’t need to report gifts out of surplus income to HMRC when they are made. In most cases, the exemption is only claimed after death, and it is up to the executors to show that the gifts met the rules.

The main exception is where regular gifts are made into a discretionary trust. If, without the exemption, those gifts would trigger an immediate inheritance tax charge, they must be reported at the time. HMRC will then confirm whether they accept that the gifts qualify as normal expenditure out of income.

For all other gifts, the claim is usually made by the executors, which requires details of income, spending and gifts for the seven years before death. This is why good record keeping really matters. Clear records, ideally supported by a written financial plan, make it much easier for executors to show that the gifts were regular and genuinely made from surplus income. Without that paperwork, even well intended planning can be difficult to defend.

Using ISA income to make lifetime gifts

Many people hold ISAs that have been left largely untouched, with any dividends or interest automatically reinvested. While this supports long term growth, it can mean surplus income is effectively being “locked away” and not used for gifting.

One option is to switch the ISA to an income mandate. This means the underlying investments are selected or structured to produce a natural yield, such as dividends or interest, that is paid out rather than reinvested. Although the income remains tax-free within the ISA, receiving it as cash makes it available for spending or gifting.

This approach can help create an ongoing stream of surplus income that can be gifted on a regular basis, potentially qualifying for the exemption and immediately falling outside the estate for inheritance tax purposes. Importantly, this does not require encashing the ISA or eroding the underlying capital.

As always, professional financial advice is key. An adviser can help assess whether an income strategy is suitable, structure gifts in line with HMRC expectations, and ensure robust records are maintained to support any future claim.

Is this right for you?

In the face of frozen inheritance tax thresholds and wider reforms, gifting out of surplus income can be a highly effective way to reduce future IHT while supporting loved ones during your lifetime.

That said, the exemption is detailed and evidence driven. Clear planning, consistent gifting and careful record keeping are essential to ensure the relief stands up to HMRC scrutiny. With professional advice, gifting out of surplus income can form a core part of a robust estate planning strategy, helping to protect family wealth as the inheritance tax net continues to widen.

Inheritance tax and estate planning rules can change. The value of tax benefits depends on individual circumstances. The FCA does not regulate tax, trust or estate planning.

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.