Author:

Jordan Gillies

Head of Business Development and Marketing,

Saltus Asset Management Team

Reviewed by: Megan Jenkins, Chartered Financial Planner, Saltus Asset Management Team

Feeling the squeeze? You’re not alone. More and more people are facing the same challenge – balancing their own retirement needs while financially supporting both ageing parents and adult children. For some, this means making tough choices and sacrifices; for others, it’s about managing significant wealth and understanding complex tax rules.

Whatever your situation, the common thread is this: With the right planning and financial advice, it’s possible to manage these competing demands without compromising your financial security.

Understanding the UK sandwich generation

Coined in 1981 by social worker Dorothy Miller, the term ‘sandwich generation’ describes those supporting aging parents and adult children – often without receiving reciprocal support themselves.[1] With longer life expectancies, rising care costs, and adult children staying financially dependent for longer, the result is a growing financial squeeze. According to the Office for National Statistics (ONS), almost 1.4 million people in the UK fall into this category.[2] Reports indicate that balancing these dual responsibilities can be particularly taxing on mental health, with many experiencing heightened stress and emotional strain. Given these challenges, seeking professional financial advice can often be helpful in clarifying priorities and support long term resilience for both the individual and their family.

Our latest Saltus Wealth Index (September 2025), a biannual survey of more than 2,000 people with over £250,000 in investable assets, tracks the financial confidence, attitudes, and priorities of the UK’s affluent. It reveals that 76% of high net worth individuals are providing financial support to adult children (18 and over), 42% to grandchildren and 56% to ageing parents or grandparents. A notable 22% are supporting both children and parents at once.[3]

These commitments aren’t trivial. Average annual gifts amount to £5,560 to adult children, £7,081 to parents, and £4,056 to grandchildren. And, as revealed in the Saltus Wealth Index, many are funding this generosity by selling investments or dipping into pension pots – decisions that can have long term financial consequences unless carefully managed.[4]

Financial pressures and risks

When you’re balancing the demands of supporting adult children and caring for ageing parents, wealth alone isn’t always enough. It’s not just about how much you have but when you need it and how easily you can access it. Without a plan, competing demands can quickly disrupt a well-structured portfolio.

Some key pressures and risks to consider in intergenerational wealth planning:

- Dual dependency drain: Helping two generations simultaneously, without a plan, can drain cash flow fast. Withdrawals at the wrong time can erode compounding and reduce future pension contributions. It’s often not the generosity causing the damage, rather it’s the timing – spending today what was meant to grow for tomorrow.

- Rising cost of care: People are living longer, often with increasing medical and care needs. Without proper planning, costs can quickly escalate.

- Tax pressure: Liquidating or gifting assets to support family can trigger significant inheritance tax (IHT) or capital gains tax (CGT) liabilities. Working with a financial adviser can help you navigate these complexities and help you make more tax-efficient decisions.

- Inflation: Everyday costs such as education, healthcare and housing often rise faster than the official inflation rate. Over time, this can erode the real value of your savings or retirement income, so it’s worth reviewing your long-term plan regularly to keep it on track – financial advice can prove invaluable here, particularly where you may have multiple dependents.

The benefits of cash flow planning

If you’re feeling squeezed by the financial demands of ageing parents and adult children, it can be hard to know what to prioritise and how those choices might affect your long term future. This is where working with a financial adviser and creating a cash flow model can be incredibly useful.

Unlike a static budget, cash flow planning can help you see how today’s decisions affect tomorrow’s wealth. A well-structured plan can help you understand the trade-offs and sacrifices required to maintain support for loved ones without jeopardising your own retirement goals. With professional guidance, your plan can adapt to life changes such as fluctuating income, unexpected expenses, or market volatility. A cash flow plan will take into consideration things like:

- Adult children’s expenses – school fees, extracurricular activities, university costs

- Parental support – healthcare costs, assisted living, home modifications

- Everyday costs – household bills, mortgage, pension contributions, holidays

- Major milestones –downsizing, gifting, retirement timing

It can also help you map out different scenarios. For example:

- What if you retired at 60 vs 65?

- What happens if a parent needs additional care sooner than expected?

- Can you afford to help your child with a house deposit without affecting your own retirement? If it will affect your retirement, in what ways?

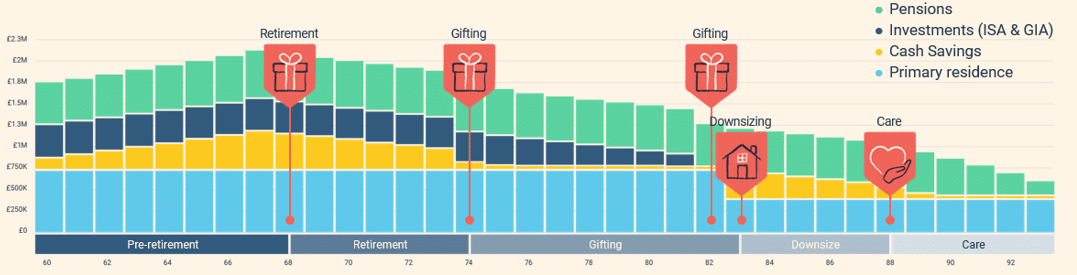

At its core, a cash flow plan allows you to make informed decisions based on real data. A simple version might look something like this:

The Financial Conduct Authority does not regulate cash flow planning.

Tax efficient wealth planning

If you have enough capital to support ageing parents and adult children without feeling squeezed, the challenge often isn’t affordability but rather the complexity. Without careful planning, you could miss opportunities to support your loved ones while also reducing tax, protecting your assets, and passing on wealth efficiently. This is where financial advice becomes essential.

If you’re in this position, there are a number of tax-efficient vehicles and strategies worth considering – each requiring careful planning and professional advice.

Gifting

Each tax year, you can take advantage of a £3,000 annual gift exemption, allowing for the transfer of assets without inheritance tax implications.[5] Larger gifts are classed as potentially exempt transfers (PETs) and fall outside your estate if you survive seven years after the gift.[6] There is also a small-gifts allowance of up to £250 per recipient per tax year, provided it’s not combined with the £3,000 exemption for the same individual.

Trusts

Trusts can be versatile tools for both control and tax efficiency, though not every structure suits every family. Professional advice is essential.

Discretionary trusts can be a useful solution for intergenerational wealth planning. All future growth is held outside the settlor’s estate, making them particularly effective for IHT mitigation. Importantly, they also offer protection against divorce, creditors and other external risks.

Interest in possession (IIP) trusts can suit families supporting multiple generations. One beneficiary, often a spouse or elderly parent known as the life tenant, receives income for life, while capital is preserved for adult children.[7] The life tenant pays tax on income; the underlying assets generally remain within the settlor’s estate for IHT purposes.

Family Investment Companies (FICs)

For families with over £2 million in investable assets, a FIC can be an effective structure for managing, growing, and transferring wealth. FICs can hold diverse assets, including property and investments, and issue different share classes to separate voting control (Type A shares) from financial benefits (Type B shares). This structure enables founders of the FIC, who may be a sole individual, a married couple or civil partners, or two or more senior family members, to retain decision-making power while distributing profits to other shareholders.

However, FICs are complex and must be set up with legal and tax advice. Ongoing administration, valuation, and reporting requirements can be significant. You can read more about Family Investment Companies here: Family Investment Companies (FICs) : A complete guide | Saltus.

Venture Capital Trusts

VCTs offer tax-efficient investment in smaller UK companies, providing 30% upfront income tax relief if held for at least five years. Dividends are tax-free, and there is no CGT on disposal.[8] However, the relief is capped at £200,000 per tax year and only applies if you have sufficient income tax liability. That said, they are very high risk, and you should speak to a financial adviser to understand whether they’re right for you. VCTs are generally suited to high earners who have already maximised other tax efficient investments like pensions and ISAs.

The Financial Conduct Authority does not regulate tax advice. In addition, the Financial Conduct Authority does not regulate tax planning or trusts.

Maintaining financial resilience

Supporting family while building your own retirement plan demands balance and foresight. According to the Saltus Wealth Index, high net worth individuals’ retirement expectations often exceed their current savings trajectory.

Pension contributions are often falling short of the full annual allowance (£60,000), with a third (30%) of respondents contributing £20,000 or less, 32% contributing between £20,000 and £40,000, and only 10% contributing the full amount.[9]

For some families, this shortfall reflects the squeeze of competing priorities, which can erode the capacity to save for retirement. In these cases, financial planning provides clarity around trade-offs, ensuring that any sacrifices made today are intentional and their potential impacts are well understood.

For others, managing multiple generations’ needs while navigating the interplay of pensions, trusts, and tax-efficient vehicles requires careful orchestration and can feel overwhelming. Even with ample resources, without a clear structure, it can be easy for opportunities to be missed and for long term plans to drift off course.

In both situations, a tailored cash flow plan and a trusted adviser can help you support loved ones responsibly, optimise your wealth across generations, and remain on track to achieve the retirement and legacy you envision.

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.