Author:

Ella Boyd

Financial Commentator,

Saltus Asset Management Team

Reviewed by: Megan Jenkins, Chartered Financial Planner, Saltus Asset Management Team

One of the more debated measures in the October 2024 Autumn Budget was the Government’s proposal to change Agricultural and Business Property Relief. For farmers and business owners, the implications would likely be far-reaching.

The original announcement confirmed that from April 2026, 100% relief on qualifying assets above £1 million would be reduced to 50%, resulting in an effective inheritance tax rate of 20%.[1] After significant industry response, the Government revised its position in December 2025.[2]

What are the current rules for Agricultural and Business Property Relief?

Currently, Agricultural and Business Property Relief (APR and BPR) can reduce the amount of inheritance tax (IHT) farmers and business owners pay.

- APR: Relief on agricultural land and buildings used for farming. It can be 100% or 50% depending on how the land is used (actively farmed or let under a qualifying tenancy).[3]

- To qualify for APR, the land must have been owned and actively farmed for 2 years prior to the transfer or date of death. Or if the land is let to someone else to farm, then it must be held for 7 years prior to the transfer or date of death.

- BPR: Relief on qualifying business assets such as a trading business, unlisted company shares, or business property like land, buildings or machinery used in trade. It can also be 100% or 50% depending on the type of asset.[4]

- To qualify for BPR, the business usually must have been owned for at least two years before death or transfer.

- There is currently no overall cap on how much APR or BPR can reduce IHT. As long as the qualifying conditions are met, relief can reduce IHT to zero on eligible assets where the full rate applies.

- APR and BPR cannot both be claimed on the same asset. You must choose the appropriate relief for each item. It can be complicated, so financial advice is recommended.

As mentioned, these rules apply up until 5 April 2026. From 6 April 2026, there will be new caps and limits on the amount of relief available. This has been discussed further below.

What has changed to Agricultural and Business Property Relief?

On 23 December 2025, the Government confirmed revisions to its original proposals.[5]

From 6 April 2026, Agricultural Property and Business Property Relief will no longer give unlimited 100% inheritance tax relief on qualifying assets. Instead, 100% relief will apply only up to a new threshold of £2.5 million per person (increased from the previously announced £1 million). Any qualifying agricultural or business assets above £2.5 million will receive 50% relief. This means they will be taxed at an effective IHT rate of up to 20% rather than the usual 40%.

The £2.5 million allowance is transferable between spouses or civil partners, who can pass on up to £5 million of qualifying farm or business assets with 100% relief, on top of existing nil-rate bands. This effectively means a married couple or civil partners can pass on qualifying assets worth up to £5.65 million tax free by combining two £2.5 million agricultural/business property allowances and, if available, two £325,000 nil‑rate bands. This transferability applies even if one spouse died before the new rules were introduced.

The change softens the original reforms, reducing the number of estates expected to be affected in 2026–27 from 375 to 185.[6]

Steps to consider next

If you think this will affect you, now may be a good time to speak to a financial adviser. While seeing an increase in the threshold is a positive, it is unlikely that further reforms will occur.

If you haven’t done so already, a good first step is to start getting a clear picture of your finances. This includes getting a handle on the value of your agricultural and business assets and how much falls within the £2.5 million (or £5 million for couples) 100% relief threshold.

You may want to consider ownership and succession planning, like ensuring assets are held by the right people, making use of spousal transfers, or passing on assets during your lifetime where appropriate (bearing in mind the two year ownership rules). In addition, reviewing business structures, partnership agreements, and wills is also important to ensure the reliefs can be fully claimed. You may also wish to consider options such as paying IHT in instalments, life assurance or ensuring you set aside enough liquid assets.

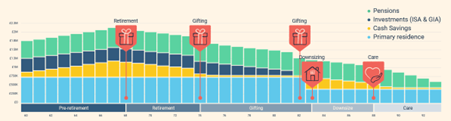

If you have a significant estate, cash flow planning can be particularly useful. Working with a financial adviser, you can model how any inheritance tax due above the threshold might be paid, while also taking account of your retirement plans and other major life events, such as gifting or downsizing. A simple version may look something like this:

As discussed, taking financial advice is key as small changes in structure and timing can make a difference.

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.