Should you always buy local?

Many investors naturally lean towards what they know, favouring shares and bonds from their home market. This tendency – known as home bias – is a result of traditional beliefs that you will benefit from investing in a familiar market; one with the same currency, same time zone, same language, and companies that an investor has grown up with.[1]

Given the globalisation of capital markets that has taken place over the last few decades, none of these traditional beliefs hold true now. Indeed, for UK investors, home bias has come at a cost over the past decade. Buying local has often meant missing out on stronger returns elsewhere, particularly the US market.

At Saltus, one of the core tenets of our investment approach has been to avoid a home bias. We believe that a home bias leads to over-exposure to one market and therefore introduces unnecessary risk in portfolios. We have always had a global approach, which has increased diversification, and risk-adjusted returns.

Our portfolios currently have a neutral position in UK equities, in line with the global stock market. Given the UK stock market’s strong performance this year, and some potential tailwinds, we are considering our allocation here. In this article we explore whether these tailwinds are sustainable, or whether the UK market performance is sending false signals.

Value or illusion?

At first glance, the UK stock market, particularly the FTSE 100, appears to offer good value. Share prices are trading at relatively low levels compared to company earnings, dividend yields remain attractive, and investor sentiment has been subdued for some time. For many, this combination suggests a potential buying opportunity.

However, a closer look reveals a more complex picture. Beneath the surface, structural weaknesses in the UK economy, uncertain global conditions, and compressed valuations may be masking deeper risks. What seems like value may in fact be a value trap.

FTSE flying high

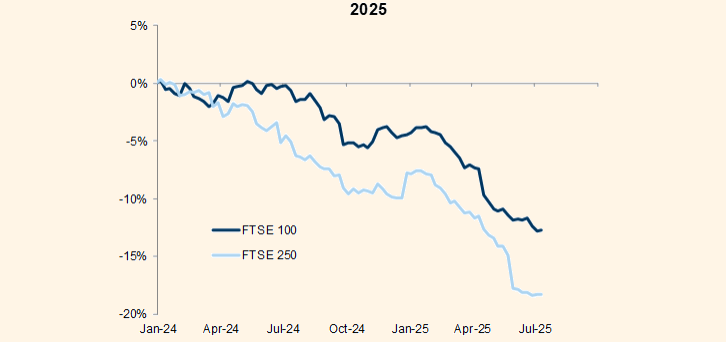

On 14th July 2025, the FTSE 100 broke through the 9,000 mark for the first time.[2] It then briefly touched an all-time high of 9,158 on 24th July 2025. Year to date, the index has risen by 10%, outpacing the S&P 500, which is up about 6.5% and 0.9% for a pound sterling investor.[3] [4]

This rally has been driven primarily by aerospace and defence companies, as well as financials. An early UK/US trade deal helped, as well as announced government reforms to boost investment in UK assets. There have also been questions over US exceptionalism (more can be read about this here: 2025: The story so far… | Saltus), so investors have redirected some of their capital back over the Atlantic.

Much of this strong performance has come from a handful of large, internationally focused companies. In fact, over 80% of revenues generated by FTSE 100 firms come from outside the UK. [5] This means the headline index is often more reflective of global trends than of the UK economy itself. As a result, while the FTSE 100 may look strong on the surface, it does not necessarily reflect the more fragile state of the domestic market. The next 250 largest companies represent a more accurate picture of the domestic market. The returns of these companies – the FTSE 250 – have been more modest, with a 5.5% gain during 2025 so far.[6]

Are UK stocks still cheap?

On paper, UK equities still look attractively priced compared to global peers. The market trades at a lower forward price-to-earnings (P/E) ratio than both the US and many other developed regions. This makes it appear like a potential bargain.

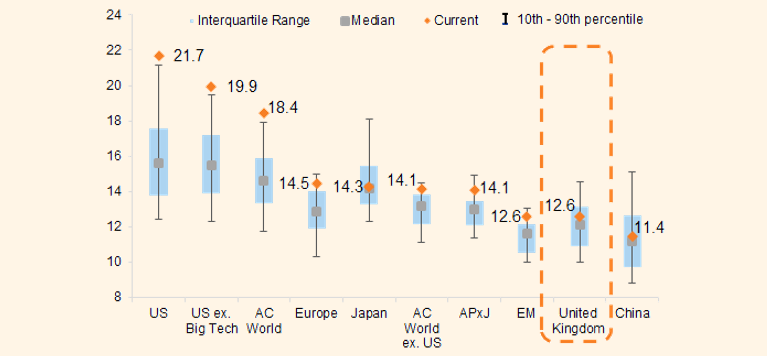

The chart below highlights the contrasts in valuations. It shows the P/E ratio of different global stock markets. The orange diamonds are the current P/E ratios. When looked at through this lens, only the Chinese market is cheaper. The US has a P/E ratio almost twice that of the UK. This suggests that from a valuation perspective, UK equities may offer more attractive future returns than their US counterparts right now.

Source Goldman Sachs Research

However, this discount comes with important caveats.

While valuations may look cheap, they are set against a backdrop of weaker earnings growth. In other words, UK companies are not generating the same pace of profit growth seen in other major markets. This is a key reason for the lower multiples.

Another red flag comes from recent earnings revisions. Earnings forecasts for UK companies have been downgraded. By contrast, earnings expectations in the US and other global markets have been revised upwards, pointing to stronger momentum elsewhere.

The chart below highlights how company earnings forecasts have been revised downwards over time. The chart highlights more negative revisions for the domestically focused FTSE 250 vs the FTSE 100.

Source: Goldman Sachs Research

So, while the UK market may still be described as “cheap” by traditional metrics, there is a good reason for this. Much of the perceived value may already be reflecting weaker growth prospects, leaving investors with limited cushion if profit margins shrink or economic conditions deteriorate.

Sluggish outlook for earnings

The outlook for earnings growth in UK companies is, at best, modest and at worst, underwhelming when compared with global peers.

Recent forecasts suggest that UK earnings are likely to lag behind those of other developed markets. This comes as domestic economic momentum remains sluggish. While the Office for National Statistics (ONS) reported a small rise in retail sales of 0.9% in June, this was from a relatively low base, and overall consumer confidence has continued to weaken. Concerns about higher taxes and persistent inflation are weighing on household spending. [7]

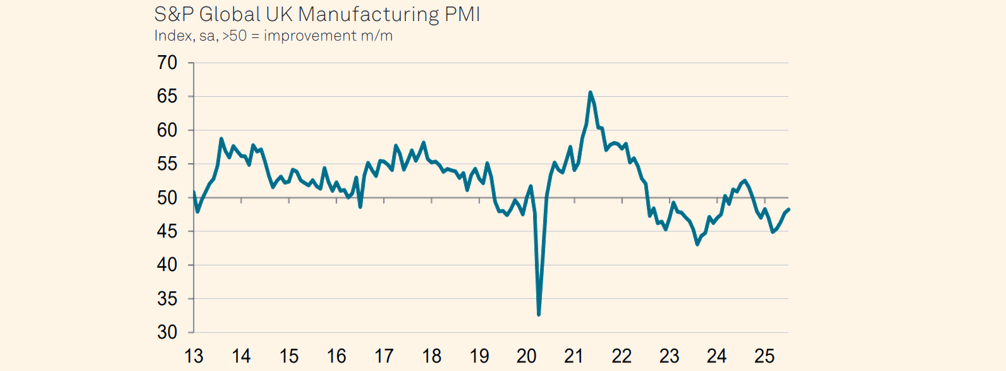

Other economic indicators paint a similarly downbeat picture. Surveys of business activity, such as the Purchasing Managers Index (PMI), have pointed to slowing growth, with falling manufacturing orders and signs of pressure on employment. A PMI less than 50 shows a contraction in the wider economy. All these trends suggest that underlying demand in the UK economy remains fragile.

Source: S&P Global [8]

Put simply, without a sustained economic recovery, or improving profit margins, prospective earnings growth for UK equities remains weak. When growth is hard to come by, even apparently “cheap” companies may not deliver the returns investors hope for.

Structural challenges

The UK stock market faces several deeper, longer term challenges that aren’t always obvious from headline performance alone.

One of the biggest is the shrinking number of public companies. Over the past year, an increase in private equity takeovers has seen a growing number of well-run, mid-sized UK businesses delist from the London Stock Exchange. This trend accelerated in 2025, reducing the depth and diversity of companies available to investors and leaving the market more dependent on a smaller group of large firms.

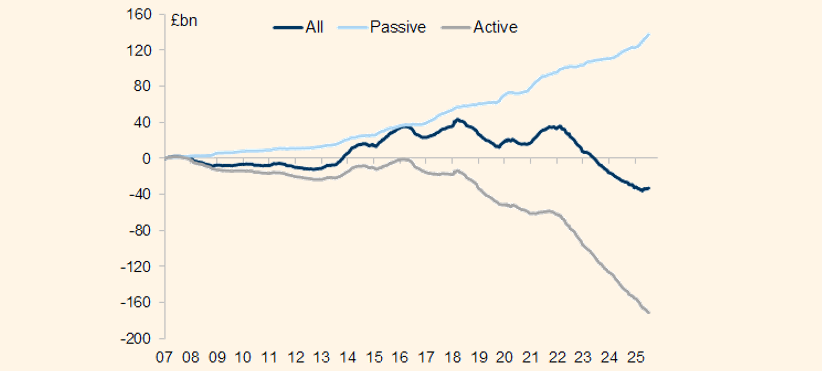

At the same time, UK pension funds and institutional investors have significantly scaled back their exposure to UK equities. This low level of home-market support means that UK stocks lack the strong domestic backing that helps provide stability during periods of volatility. The graph below shows investor flows into the UK market. The dark blue line indicates that there have been net flows out of the UK likely into global equity markets or into other asset classes such as bonds.

Source: Goldman Sachs Research

What this means for investors

Given these risks, it may be time for investors to take a more considered and targeted approach to UK equities. Rather than gaining exposure through broad indices, there may be greater value in focusing on select companies with strong balance sheets, steady cash flows, and global growth potential. These firms are more likely to weather economic headwinds and deliver consistent performance over time.

You can read about our investment into a UK infrastructure fund here: Asset allocation update August 2024 : How we’re thinking about markets… | Saltus.

Diversification remains an important tool. With the UK market facing its own unique set of challenges, balancing domestic holdings with international equities, fixed income, and alternative assets can help manage risk and smooth returns. Investors might also consider placing greater emphasis on governance and corporate resilience. As more UK firms are being taken private, identifying those that remain publicly listed with strong, transparent leadership becomes increasingly important.

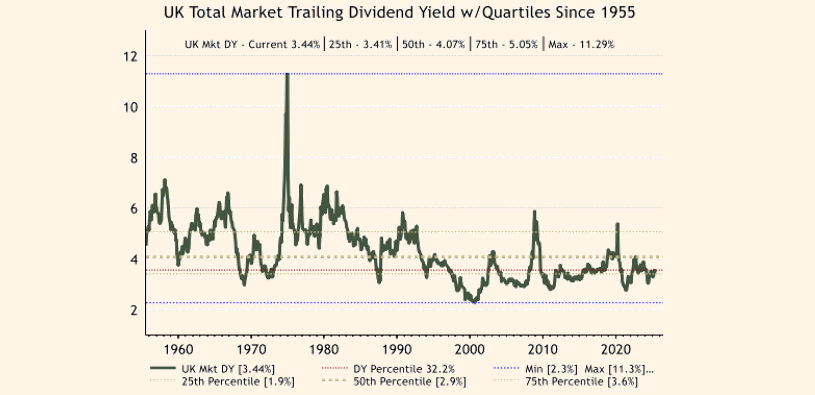

Caution is also warranted when it comes to dividends. High yields are appealing, especially in a low-growth environment, but not all are sustainable. Investors should seek out companies with the financial strength and earnings stability to support their payouts over the long term. Lastly, it’s crucial to remain aware of global events. From trade negotiations between the US and EU, to monetary policy shifts at the Bank of England, these developments will continue to influence how UK equities perform. The below chart shows how UK stock market dividend payout is significantly lower than historical averages.

Source: ASR

The bottom line

At a glance, UK equities may appear to offer a compelling investment opportunity: cheap valuations, high income, and a contrarian story. But when viewed in full, the picture is far more complex. Weak domestic growth, a shrinking pool of publicly listed companies, overreliance on global sectors, and fragile investor support all point to a market that may not be as undervalued as it seems. What presents itself as value may in fact be a trap. For investors, distinguishing between the two could make all the difference.

In recent years, many UK investment firms have reduced their exposure to UK equities as the relevance of a home bias has been called into question. Most are still far above the global stock market weighting in the UK though, and so over-concentration of portfolios remains.

At Saltus, we take a more progressive view. Global diversification and an unconstrained approach lie at the core of our investment philosophy. We don’t just tweak around the edges, we focus on identifying the best opportunities wherever they arise, without being tied to arbitrary benchmarks.

Our investment range is the result of a disciplined process and rigorous manager selection, designed to help our clients navigate complex markets with confidence.

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.