Investment conditions

Growth (economic)

The key issues investors are grappling with are economic ones: is inflation under control? Are economies holding up? Will we see recessions, and if so where, and what shape will they take? Will geopolitical tensions worsen the outlook? What do these mean for the path of interest rates and what investments are likely to prevail? Taking these in turn…

Inflation has fallen a lot over the last year. For example, comparing March 2023 to March 2024 CPI numbers, inflation has gone from 10.1% to 3.2% in Britain, and 5% to 3.5% in the US. Some shorter term inflation numbers have increased in the US to north of 4%, which investors have focussed on very recently, but generally, the inflation outlook is much better now than it was a year ago. The IMF expects global inflation to fall from 6.3% in 2023 to 5.9% in 2024 and 4.5% in 2025.

Despite continued (but slower) price rises and lingering geopolitical tensions, most economies are holding up. Gross Domestic Product (“GDP”) readings essentially quantify how much stuff is produced and sold in an economy in a given period (services as well as goods). GDP readings show a mixed bag, but in the main are significantly stronger than many predicted would now be the case. Selected recent GDP readings are: USA 3.1% current (1% a year ago), Britain -0.2% current (0.4% a year ago), Euro area 0.1% (1.8% a year ago), Japan 1.2% (0.4% a year ago), China 5.3% (4.5% a year ago).

Looking ahead, the IMF expects the world economy to grow at 3.2% in 2023, 2024 and 2025. Below the historical (2000-19) average of 3.8%, but positive growth nonetheless, i.e. not in recession.

Unemployment remains near historic lows in the USA (3.8%), Britain (4.2%), Euro area (6.5%), Japan (2.6%), and China (5.2%). Labour markets remain strong in our view.

Leading indicators are used to forecast future economic activity, one of the most popular being Purchasing Manager Indices (“PMIs”) which are monthly surveys of business executives who make orders for their companies. Readings below (above) 50 indicate economic contraction (expansion). The latest PMIs for various regions are Global (50.6), US (50.1), UK (50.3), Japan (48.2), Europe (46.1), Emerging Markets (52).

Geopolitics continues to present a risk. The committee acknowledges a lack of informational advantage in this area, it doesn’t pretend to know what will happen. For now, economic impacts appear to be known and manageable on a global basis, even if very damaging in some isolated cases. We remain watchful and ready to respond to emerging threats. For more information on politics and markets please read this recent article: https://www.saltus.co.uk/investment-management-insights/elections-politics-financial-markets-and-investment-portfolios

Interest rate & liquidity environment

Most major economies have been raising interest rates in an attempt to cool inflation. However, interest rates are not expected to move much higher because inflation has been falling. The committee thinks the worst of the hiking cycle is behind us. That said, the risk of a policy mistake by central bankers is elevated in our view. Reduce rates too soon and inflation could rise again, as was the case in the 1970s/80s. But keeping rates too high for too long could damage companies and consumers with high debt levels. This is a difficult balancing act, especially since the impact of higher rates generally takes 12 to 24 months to be felt.

Recent inflation numbers out of the US were higher than expected, above the long-term target inflation rate. Because of this, and because economic growth is fairly strong, investors expect US interest rates to stay higher for longer than was expected at the start of the year.

Valuations & earnings outlook

At the global level, corporate earnings have been resilient, and higher than expected in many areas. Global profit margins have remained robust, despite rising prices and borrowing costs.

Company earnings expectations are broadly positive and improving. At the global level, analysts expect 9.3% earning growth in 2024 and 12.7% in 2025. At the regional level, analysts expect good corporate earnings for the US (+9.7% 2024 +13.9% 2025), Japan (+8.7% 2024 +8.8% 2025), and Emerging Markets (+19.8% 2024 +15.5% 2025). Earnings expectations in the UK and Europe are low in 2024 (+1.6% and +3.5% respectively), but higher in 2025 (+8% and +10.3% respectively).

The US stock market is the only major region that is meaningfully overvalued compared to history, investors are prepared to pay more for companies listed in the US in general, and especially for those expected to profit most from new technologies (e.g. artificial intelligence). The UK stock market is cheap compared to history, trading about 20% more cheaply than its 10-year average (price to earnings ratio).

Sentiment / flows

Predicted stock market volatility has been fairly low over the last twelve months, the widely followed VIX index rarely edged above its long-term average of 21 throughout 2023 (currently at 16). Readings above 30 generally indicate fears of large drawdowns in stocks. Investors appear to feel more cautious now than they did at the start of this year, with stock market volatility having increased following recent macro-economic results. There remains lots of demand for riskier bonds, which shows either a continued belief in the strength of the underlying companies, or complacency.

Views by asset class

Equities

Measures of global stocks show good gains year to date. However, returns have been flattered by a few very large companies experiencing very large gains, mainly attributable to expected revenue growth from artificial intelligence (e.g. Nvidia +70.7% year to date!).

Mindful of how expensive these technology companies have become, and in an effort to avoid potentially large drawdowns from expensive stocks (as has happened several times over the last 50 years, most notably Nifty Fifty in the 1980s, and the dot-com bubble of the late 1990s), the asset allocation committee has had less exposure to some of these companies than would have been optimal for clients. The committee reassessed our logic and maintained our slight underweight to big tech – we do have exposure but less than we could have. Instead, the asset allocation committee has been focussing on less expensive companies, those with greater margin of safety in their stock price. So far this year this has detracted from performance, but is done in an effort to safeguard investor capital.

For some time now, the committee has been tilting stock portfolios towards “quality” companies, those with stronger balance sheets and less volatile earnings. This has been very beneficial for portfolios. In the most recent meeting, the asset allocation committee decided to maintain our preference for “quality” stocks.

Among developed markets, whilst our largest country exposure is in the USA, we also express a preference for Japanese equities, given the ongoing accommodative policy, presence of negative real interest rates, and the implementation of shareholder-friendly reforms that are taking hold. Returns in US equities have been good over the last year, they’ve been even better in Japan. The committee decided to bank some of the profits in Japan and deploy the capital into Emerging Markets which are significantly cheaper because of the recent gains in Japan.

We had recently increased exposure to Asia, emerging markets, and frontier markets. This decision has contributed meaningfully to investment portfolios. Many of these countries are ahead of developed markets when it comes to growth and recovery, they haven’t had the same cost increases as some Western countries and have been trading more cheaply than many developed markets. Because of more positive news out of China, the committee decided to increase exposure to Asia and emerging markets (preferring to play China via these proxies rather than having direct Chinese exposure).

We remain unconvinced about the case for European equities, given uncertainties over many factors in the region, such as concerns about debt sustainability and low growth. Because of the uncertainties, our exposure to European stocks comes mainly via a long/short equity manager, because they can generate returns from both rising and falling stock prices, they’ve generated +10.4% year to date.

Overall, we continue to tilt our equities towards quality companies (those with higher returns on equity and who are typically more resilient when the outlook deteriorates), and smaller companies (which are trading more cheaply than the average stock).

Government bonds

The last two years were the worst two-year period in 150 years for US government bonds, and UK government bonds recently lost about a third of their value over a three year period (conventional all stocks UK Gilts recently fell -35%). We have been increasing our exposure to these investments but were slightly early on this call. Government bonds recently fell in value because inflation hasn’t fallen as quickly as some hoped. But the losses are manageable and the asset allocation committee are comfortable with their inclusion because they yield over 5% and because if equities have a correction then these bonds could provide some protection.

Corporate bonds

The committee have been increasing client exposure to corporate bonds and emerging market bonds. These have performed well since the decisions were made. Because many of these bonds have risen in value, they are less attractive now compared to other investments. So in the most recent committee meeting, the committee decided to take some profits on these bonds and increase exposure to Alternatives.

Alternatives

Alternative asset classes can provide returns not correlated to stocks and bonds, providing additional sources of growth or protection. For this reason, we are still positive on this asset class and the committee decided to increase our exposure in the most recent meeting.

We have positions in broad commodities as well as copper, all of which look undervalued on a long-term view. We have some macro hedge funds that can add significant value in times of heightened volatility. We also have positions in gold and gold miners, gold can provide meaningful protection when inflation surprises on the upside, and gold miners are significantly undervalued in our view.

Summary of positioning

Below is a summary of our views for each asset class, from strongly negative (- -) to strongly positive (+ +).

Asset Class

| Asset class | -- | - | Neutral | + | ++ |

|---|---|---|---|---|---|

| Equities | X | ||||

| Government bonds | X | ||||

| Corporate bonds | X | ||||

| Alternatives | X | ||||

| Cash | X |

Asset Class Breakdown

| -- | - | Neutral | + | ++ | ||

|---|---|---|---|---|---|---|

| Equities | USA | X | ||||

| UK | X | |||||

| Europe | X | |||||

| Japan | X | |||||

| Asia ex-Japan | X | |||||

| Emerging markets | X | |||||

| Bonds | Government | X | ||||

| Index-linked | X | |||||

| Investment grade | X | |||||

| High yield | X | |||||

| Emerging market | X | |||||

| Convertibles | X | |||||

| Structured credit | X | |||||

| Alternatives | Commodities, gold + miners | X | ||||

| Macro hedge + other alts | X |

Investment Committee Q&A

In this feature we attempt to lift the lid on the process and our views by interviewing one of the decision-makers: Andrew Fleming: Chairman of Saltus Asset Management and the Asset Allocation Committee

The Committee last met two months ago, what has happened since then?

Riskier assets performed well in the first quarter of this year. However, both equities and government bonds fell in value in April following economic announcements out of the US. Since their recent falls, equities have recovered much of their earlier poise. Within bond markets, credit has continued to perform well as expectations for a recession dissipated, we had recently increased our exposure.

What has been driving investment markets in this period?

The key continues to be the performance of and expectations around the US economy and macro environment. Economic momentum has been strong through 2023 and has continued into this year. That said recent data, at least at a headline level, has challenged the consensus of strong economic growth combined with slowing inflation sufficient to allow the US Federal Reserve to start to cut interest rates later this year and into 2025. The culprit was the quarter 1 2024 US real GDP data which looked as if conditions may be more ‘stagflationary’ than market participants were anticipating. The key numbers were quarter on quarter economic real GDP growth of 1.6% against 3.4% on the same basis in the previous quarter, combined with inflation as measured by the GDP deflator coming in at 3.4% for the first quarter against 1.8% in the fourth quarter last year.

What has been working well for our portfolios, and what has been less effective?

In December we increased our weightings to equities. This was very positive, particularly in higher risk mandates. Our positions in US and Japanese equities, as well as some of our alternatives (e.g. gold, commodities and copper) have been very positive. In lower risk mandates, holdings in government bonds have detracted but been offset by good positions in credit instruments. Overall having made the no recession call last year when, as I have observed before, market consensus believed a recession was highly likely, and so far correctly anticipating that inflation would be falling into this year markets have largely supported our positioning for clients.

What decisions have the committee been making, because of the macro-economic conditions you’ve just described?

We remain very focussed on where we see the big picture underlying trends going rather than being overly driven by shorter term monthly or quarterly economic data releases. We have been of the view that this is turning into what looks remarkably like a ‘normal’ economic and macro cycle – which is a really important conclusion given how unusual the relatively recent Covid-related cycle was. If conditions were turning ‘stagflationary’, i.e low economic growth combined with elevated inflation, then the outlook for investment returns would be poor as evidenced by the 1970s, when the word was first coined, a decade when both bonds and equities were weak. Based on our view that this was looking more like a normal economic cycle we added in December to equities in general which has been very beneficial through the first quarter. There has been a pullback in both bonds and equities following the release of the Q1 GDP data but fortunately it appears to have been short-lived as in recent days both bonds and equities have recovered again. What is ‘normal’ about this cycle in the US is the housing market continues to recover, employment and real wage growth is strong driving consumption and now capital investment is in a strong uptrend with companies pivoting away from China to invest in domestic, ‘onshore’, supply chains. Business investment in plant, software, computers and R&D are all at record highs in the US. It is this investment that is beginning to improve productivity numbers which if it endures will drive equity market returns into a strong new cycle. The aspect of the current macro environment that is not normal is the scale of the US Federal Government stimulus through its ‘onshoring’ subsidy regime and running a significant deficit at a time of strong private sector growth, and therefore tax receipts, which is highly unusual. In this sense policy in the US increasingly resembles that of a war economy with the US administration and policy establishment taking on China. The bi-partisan vote to force Chinese company ByteDance to sell Tik Tok is a prime example of consensus among US policy makers when they agree on so little else. We also believe inflation will continue to fall to the 2.5 to 3% range which will allow central banks to reduce interest rates into next year even if shorter term market rate cutting expectations probably got a bit ahead of themselves.

The FTSE 100 just reached an all-time high. What’s behind that?

The FTSE 100 recent attainment of a new all-time high has received a lot of press attention in the UK. We would point out that the FTSE 100 is not very representative of the UK economy and is dominated by large multinationals much of whose earnings are in non £ currencies. The index in US $ terms, for example, is still well below its all-time high as the strength of the FTSE is largely a reflection of weakness in sterling. Flows out of UK equity funds continues relentlessly as UK investors increasingly adopt a more global stance, something we put in place some time ago. If the US economy and productivity cycle falters then UK equities will be a beneficiary given its deep ‘value’ characteristics as US equities are undoubtedly expensive although earnings growth remains low in the UK. There are potentially some catalysts for UK equities performing better: more bids from private equity and trade buyers, corporate buybacks and longer term changes to the savings environment. Meanwhile sterling has again recently been weaker in line with a relentless long term trend as the potential for interest rate cuts by the Bank of England ahead of the US Federal Reserve rises, which, if it happened would be highly unusual.

It feels like the temperature of geopolitics has been rising. How worried are you about this from an investment perspective?

We have observed before there is plenty to worry about in the World particularly from a geopolitical perspective. Generally this is probably exacerbated by the 24 hour news-driven world we inhabit today. What is different today is the war in Ukraine which pitches Russia supported by China against a NATO-supported ‘western’ proxy and the Israeli/Hamas conflict in Gaza overlain with the epochal battle between the US and its allies vs. China. We try to look through the geopolitical tensions as it is effectively impossible to get clear insights to focus on the underlying macro, economic and liquidity environment. So far the World trading system is holding up well under the strain and the structure of capitalism and innovation that drives productivity and corporate earnings growth is still largely intact.

We’ve had larger allocations to Japan than most, what was the reason for that?

Our large overweight through last year in Japanese equities has served our clients well. Over the last twelve months global equities as measured by MSCI World have risen by c21% in local currency terms with Japanese equities up by some 40% while Chinese equities, for example, have fallen by 15% on the same basis. This standout performance from Japan among the larger equity markets has been driven by strong corporate fundamentals with improving margins and strong positive earnings revisions combined with real signs that the corporate reforms designed to make quoted companies more ‘shareholder friendly’ were having a positive impact.

The committee just voted to reduce our allocation to Japan, why was that?

We are slightly trimming our Japanese holdings largely in favour of a higher emerging markets weighting as the relative improvement in earnings and generally more attractive valuations, following Japanese outperformance, moves in favour of emerging markets. We remain overall still positive on Japan, however, as more companies start to manage their businesses in the interests of external shareholders and a weaker yen supports Japanese corporate competitiveness.

Where the mandate allows, we’ve been investing in a range of commodities, can you outline the thinking behind this?

Our commodity positions have been very positive for portfolio returns this year having been a slight drag last year. We have had a long-standing exposure to commodities in general and copper in particular on grounds of structural long term demand associated with the green energy transition while supply is constrained. Our positions in gold and gold mining equities have also been helpful. Gold miners are very cheap relative to the bullion price as higher inflation in input costs depressed profitability in recent years. We believe the derating of gold mining shares has largely run its course as cost inflation falls back. The interesting thing about copper is that its price has been performing well while the oil price is relatively weaker. Traditionally these two key products with demand largely tied to the global growth cycle have risen and fallen together. We think the outperformance of copper is an early sign of structural demand and in the shorter term may be related to Chinese stockpiling battery, solar and wind-related commodities as they expand production in these sectors to try to offset the slump in the domestic property market that has savaged domestic household consumption. It also looks as if Chinese speculative demand has been responsible for the recent rise in the gold price as households seek alternative stores of value to the discredited property market combined with structural demand from the Chinese central bank which continues to build gold reserves as it tries to engineer an alternative to the US $ global financial system.

Manager in focus: Man GLG High Yield Opportunities

Summary

This fund aims to provide income and capital growth by investing in corporate bonds (loans to companies) that have a high yield.

The fund has a current yield to maturity of 8.89%, so it offers investors an opportunity to generate returns above inflation, although the yield is not guaranteed.

Bonds have a high yield when they are perceived to the riskier than safer bonds that have lower yields. But this fund has an impressive team and track record, and we are comfortable with the risks when used as part of our diversified portfolios. Should investment conditions become less favourable we would likely reduce our exposure (as we would with other risky assets such as equities).

What are high-yield bonds?

When companies want to raise money to fund their operations, many choose to borrow money from investors in the form of corporate bonds. The greater the perceived risk that the company will default on their bonds, the higher the interest rate will be, and the greater the yield for an investor (unless the company defaults).

Companies issuing high-yield bonds include smaller, early stage companies, as well as companies with relatively high levels of existing debt.

Who are Man GLG?

Man GLG is a division of the larger Man Group, which has a rich history dating back to 1783. Originally known as ED&F Man in 1869, the company went public in 1994 before becoming private again. However, the financial services arm Man Group remained publicly traded. In 2007, the company separated its brokerage arm (MF Global), maintaining Man Group as it is today.

The company operates through five main divisions: Man AHL, specialising in diversified quantitative hedge fund strategies. Man Numeric, another quantitative hedge fund division. Man GLG, focusing on active investment management. Man FRM, offering active hedge alternatives; and Man GPM, dedicated to private markets.

The High Yield fund is under the umbrella of Man GLG, which originated from GLG Partners, initially a part of Lehman before becoming independent in 2000 and later going public in 2007. Man Group acquired GLG Partners in 2010, and it is now fully owned by the larger group. Together, they manage over £45 billion in assets across various investment strategies.

Investment Philosophy

Man GLG High Yield Opportunities is a flexible global high yield bond fund managed by Mike Scott who started the fund in 2019. Mike takes a versatile approach, hunting for investment opportunities wherever they arise in the high-risk market. He identifies undervalued bonds to buy and also shorts overpriced ones, aiming to profit from price movements.

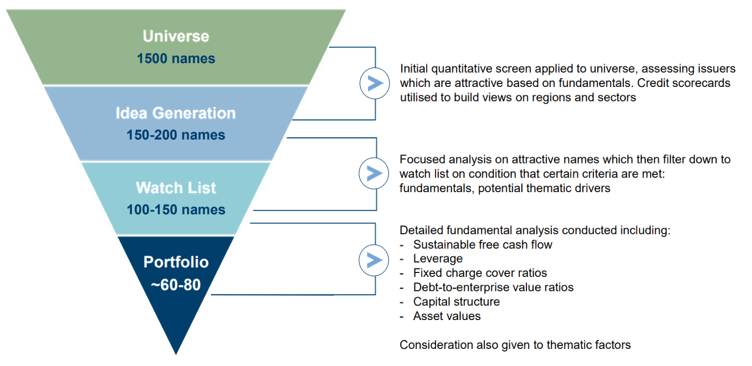

To build his portfolio, Mike begins with a broad list of around 1,500 bonds. He then narrows it down using quantitative metrics to find about 150-200 promising candidates. From there, he conducts a detailed analysis to select 100-150 bonds with strong fundamentals and favourable macroeconomic trends. He also considers broader factors like consumer trends and regulations.

The final portfolio comprises 60-80 bonds, carefully chosen based on their fundamentals. Mike weighs each position considering factors such as sector, country, liquidity, and debt seniority. He aims for a diverse portfolio that can thrive in various market conditions.

Positions are typically held for about a year, allowing for swift adjustments, especially in opportunistic trades. The fund has a turnover rate of about 75-80% which is significantly higher than funds within its peer group at 60%. So this fund is very actively managed.

At least two-thirds of the fund is invested in below investment-grade bonds. Mike seeks a mix of global opportunities, with a preference for UK, North American, and European markets. The fund is mostly hedged back to sterling, providing stability amidst currency fluctuations.

Illustrated in figure 1 below is the process used by Mike and his team.

Source: Man GLG

Performance

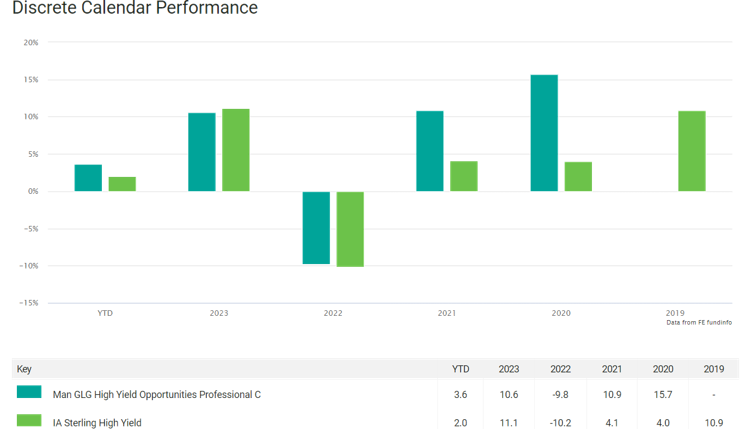

Performance has been strong over the last few years particularly when comparing the outperformance to the UK high yield market.

Figure 2 outlines the performance of the fund broken into calendar years back to 2019.

As of March 2024, the fund has returned 45% since inception of the fund in 2019. When annualised this figure stands around 7.5% and aligns within the volatility (14.5%) budgets of our higher risk portfolios.

Fig 2. Man GLG High Yield Opps Investment Performance

Source: FE Fund Info

Saltus Investment Case

- The fund provides opportunity to invest into an unconstrained strategy across the UK and Europe in the high yield space. Not only does this provide a good level of diversification to our portfolios through the use of an absolute return strategy but it also provides access to two different geographies.

- The fund’s performance stems from a closely-knit team that has collaborated for many years. Portfolio manager Mike Scott brings nearly two decades of expertise in navigating fixed income absolute return strategies. The team’s consistent approach contributes to a well-thought-out and strategic investment approach.

- Since inception, the high yield opportunities fund has demonstrated impressive performance, notably surpassing expectations with a 15.5% outperformance in 2020. The fund has consistently delivered a strong annualised return of 7.5% after fees. While past performance can be useful to visualise, it’s important to recognise that it doesn’t ensure future outcomes. Investors should remain mindful of the dynamic nature of financial markets and conduct thorough research or speak to an investment professional before making investment choices.

Saltus use this fund as part of a diversified portfolio. This is not a recommendation to invest in this fund. Saltus will not be liable for any losses incurred as a result of investing in this fund.

Asset Allocation Committee

The committee consists of several senior members of the investment team, all partners, who invest their own money alongside clients. The committee is led by:

David Cooke

Co-Chief Investment Officer , Saltus Asset Management Team