Investment conditions

Growth (economic)

Positive momentum in global economic growth continues, and it has become more broad-based. Inflation has fallen back into line with central bank targets both at a headline level and also when excluding the more volatile energy and food prices. Corporate earnings are robust, wages continue to rise, and the consumer is still active. The risk of a recession in the medium term has risen at the margin and pockets of weakness are emerging, but we believe this positive growth environment will remain in place for a while longer.

GDP growth in most major economies is positive according to second quarter data. Quarter on quarter GDP growth on an annualised basis showed a healthy 2.8% growth in the US, 2.8% in China, 3.1% in Japan, 1.2% in the Euro Area, and 2.3% in the UK. Notably, in the first six months of 2024, the UK economy was the fastest growing economy in the G7 group (the seven largest economies in the world). The IMF estimates global economic growth the be 3.2% in 2024 and 3.3% in 2025. This growth is skewed towards emerging economies, and looks slightly more subdued in advanced economies. For example the IMF estimates the US economy will grow by 1.8% in 2025, the UK and Euro Area at 1.5%, and Japan at 1%, whilst China will grow at 4.5% and India at 6.5%.

The recent surge in inflation seems to be back under control in advanced economies. July data showed annual inflation rates coming down towards target levels (2.9% in the US, 2.2% in the UK, 2.6% in the Euro Area). Whilst heading in the right direction, the inflation rate actually increased in the UK and the Euro Area between June and July, reminding us that the journey to a more normal inflation environment will not be linear, and there could still be upside surprises to come. In an environment of strong growth and low unemployment, inflation could prove to be stickier than many expect.

Leading economic indicators such as the Purchasing Managers’ Index (PMI) are still showing weakness in the manufacturing sector and strength in services sector, a trend that has been in place since economies opened up post-covid. A PMI number above 50 indicates an expansion, and below 50 a contraction. In the preliminary August data, the US manufacturing PMI fell to 48, but the services PMI was a healthy 55.2. In the Euro Area the manufacturing PMI remains weak at 45.6 (42.1 in Germany), but services stronger at 53.3. In the UK both figures are above 50, again proving the UK is in a relatively strong position economically after experiencing a technical recession in 2023.

The consumer remains robust in the face of higher interest rates and prices. Real wages are rising and unemployment is low. It will take sustained labour market weakness to start to dent consumer confidence, which will feed through into lower corporate earnings and an economic slowdown. The committee doesn’t see this as an imminent threat in the short term, but is aware of the growing risks.

Interest rate & liquidity environment

There has been notable dispersion amongst central banks and the direction of their monetary policy, which has created some volatility in financial markets.

The Bank of England joined the growing number of central banks opting for a reduction in interest rates at their most recent meeting. They join a growing group that includes Europe, China, Canada, Sweden, New Zealand and Brazil.

On the opposite end were the Bank of Japan, who opted to raise their base interest rate to 0.25% at their most recent meeting. A tiny move in absolute terms, but given rates were negative in Japan for 8 years this was significant. The decision put upward pressure on the Japanese yen as the difference in interest rates between Japan and others narrowed.

The US Federal Reserve held their base interest rate at their most recent meeting, but it is widely expected that they will start cutting at their next meeting in September.

Apart from the so far short-lived financial market volatility, liquidity in the financial system remains plentiful and financial conditions loose, even in the face of tightening by central banks. This is supportive to the current benign investment environment.

The committee remain of the view that we are entering a sustained rate cutting cycle now that inflation looks to be under control, but are aware that these cuts may be slower to materialise than what is forecast.

Valuations & earnings outlook

The second quarter corporate earnings season was stronger than expected. Analysts are now forecasting global earnings growth of 9.9% in 2024, rising to 13.6% in 2025. Within this, the US and Emerging Markets are forecast to have the fastest growth, at 15.6% and 16.1% in 2025 respectively. The UK, Europe and Japan forecast 2025 returns look more moderate at 8.8%, 10.3% and 10.2% respectively.

US corporate profit margins are near record levels and are expected to stay there into 2025. Given healthy expected earnings growth and high profit margins, US equity market valuations are meaningfully higher than their long term average on a 10 year price to earnings basis. A large part of this is driven by the ebullient technology sector. Unless already stretched valuations, earnings growth and profit margins can expand further in the year ahead, we believe there is limited room for upside in this part of the market.

Europe and the UK are cheap, and Japan and Emerging Markets fairly valued compared to their long term average multiples.

The information above is based on country level data. If you look at earnings forecasts and valuations within different parts of these markets there is more dispersion. For example within the US, smaller companies are cheaper but do not have the same level of forecast earnings growth, and cyclical stocks look expensive relative to defensive stocks, as fears of recession have subsided over the last two years. Smaller companies in Asia ex-Japan, Europe, UK and Japan have high forecast earnings growth and lower valuations. The committee discussed these dispersions with interest as they could offer attractive investment opportunities.

Sentiment / flows

Based on market data and investor surveys, market sentiment and positioning look neutral on the whole. Sentiment took a hit during the market volatility seen in early August, but has since recovered. Stock markets have positive momentum, and investors aren’t paying for protection in the options market, signalling a lack of nervousness.

In early August US stock market volatility – as measured by the VIX index – spiked to levels not seen since the covid crash. It has since settled back into its relatively low 2024 range.

Weekly flows into financial market assets have been strong over the last three months, above the average for 2024. This is based on global fund flow data.

Views by asset class

Equities

Equity markets have experienced significant volatility in the last few weeks. Weak US inflation data released in July resulted in a rotation away for the dominant US technology sector and into smaller companies. Global equity markets then fell sharply in early August, but have since made back most of these losses. The summer months tend to be more volatile for financial markets, as there is typically less liquidity which exacerbates small moves. Most major equity markets are still sitting on healthy gains for the year to date.

Despite the recent volatility, the committee’s overall view on equities hasn’t changed. The violent swings in markets in August were driven by specific factors and a consolidation in the most extended areas, and therefore haven’t warranted a meaningful reassessment of the equity market outlook.

The committee opted to maintain the equity weighting, whilst gradually increasing some of the higher conviction positions at the margin. We continue to have an intentionally lower weighting to the US technology sector given current valuations and optimistic earnings forecasts. We think there are better opportunities for upside elsewhere in the US market, which we have exposure to through the equal-weighted S&P500 index, and our active US equity fund managers.

Within the global equity allocation, we maintain a bias towards high quality companies, characterised as companies with robust balance sheets and stable profitability. The committee decided to continue adding to our defensive positions within the global equity exposure given the view that an economic slowdown could now be closer on the horizon, funding this from the more expensive, growth-exposed managers.

In other regions, we will continue to increase exposure to smaller companies in Japan. Smaller companies are more domestic-focused and so benefit directly from Japanese economic strength and corporate reforms. They are less dependent on exports which could mitigate the negative impact of Japanese yen strength. This will be funded through a cut to the larger Japanese companies, so overall the size of the exposure will not change, just the composition. The committee decided to steadily add to our UK smaller companies positions as the growth outlook and valuations in this part of the market make it an interesting place to take risk.

Government bonds

Given recent inflation data and central bank rhetoric around lower interest rates, government bond yields have fallen and their prices risen. The committee are comfortable with current exposure to this asset class, but would like to add to it at the margin where possible, as government bonds are becoming a good offset to equities again now that inflation appears to be under control. The positive portfolio effect was felt during the bout of market volatility in August when equities fell but government bonds rose considerably, resulting in a stable return through the period.

US government bonds have again been outperforming their UK counterparts, and so we will continue to move our exposure from the US to the UK because UK bonds are more attractively priced. The committee are of the view that there may be fewer interest cuts than currently forecast in the US, but more than currently forecast in the UK, which makes UK government bonds relatively more attractive from here. The committee also decided to increase the duration (interest rate sensitivity) of our government bond exposure by slowly swapping short-dated UK government bonds for longer-dated ones.

Corporate bonds

Corporate bonds have continued to perform well and support client portfolios. There is no change to this part of the portfolio.

Alternatives

What we want from this asset class is a return stream for portfolios that is uncorrelated to listed stocks and bonds, and therefore can provide key protection in times when stocks and bonds are moving down together. We are still positive on alternatives, given this useful portfolio role.

This is a varied asset class and our positions are in place to perform in a range of different market environments. At the most recent meeting the committee decided to increase our exposure to gold mining companies. The price of gold bullion has reached an all-time high, but gold mining companies still lag behind. We believe as the increased profitability of these mining companies is recognised, there is potential for them to catch up to the gold bullion price.

The committee also decided to reduce exposure to the broad commodity index and use the proceeds to increase exposure to copper. This results in a more concentrated commodity position. We think copper will be integral in an electrified future, but there hasn’t been enough investment into new supply so you could see prices rise as the resource becomes scarce.

Summary of positioning

Below is a summary of our views for each asset class, from strongly negative (- -) to strongly positive (+ +).

Asset Class

| Asset class | -- | - | Neutral | + | ++ |

|---|---|---|---|---|---|

| Equities | X | ||||

| Government bonds | X | ||||

| Corporate bonds | X | ||||

| Alternatives | X | ||||

| Cash | X |

Asset Class Breakdown

| -- | - | Neutral | + | ++ | ||

|---|---|---|---|---|---|---|

| Equities | USA | X | ||||

| UK | X | |||||

| Europe | X | |||||

| Japan | X | |||||

| Asia ex-Japan | X | |||||

| Emerging markets | X | |||||

| Bonds | Government | X | ||||

| Index-linked | X | |||||

| Investment grade | X | |||||

| High yield | X | |||||

| Emerging market | X | |||||

| Convertibles | X | |||||

| Structured credit | X | |||||

| Alternatives | Commodities, gold + miners | X | ||||

| Macro hedge + other alts | X |

Investment Committee Q&A

In this feature we attempt to lift the lid on the process and our views by interviewing one of the decision-makers, this time it’s: Charlie Ambler: Co-Chief Investment Officer.

The Committee last met two months ago, what has happened since then?

There has been a significant amount of volatility in markets over the last two months. In July, a softer US inflation print resulted in an aggressive rotation out of the US technology sector and into smaller companies. This was with an expectation that softer inflation would lead to interest rate cuts which tend to benefit smaller companies as a larger portion of their debt is floating rate. As July turned to August, the Bank of Japan surprised the market with an interest rate hike which caused the Japanese yen to strengthen. The Japanese stock market sold off violently, and shockwaves rippled into other stock markets too. Stock market volatility reached levels not seen since the covid crash in March 2020. What was perhaps more surprising though was the fact that by the end of August markets had not only recovered their composure but were sitting on gains for the month. Through all of this government bond prices rose (as yields fell) which provided useful portfolio balance.

What has been driving investment markets in this period?

The main driving forces in investment markets continue to be the path of inflation and interest rates. Recent data show inflation is almost back at central bank target levels. There are pockets of sticky inflation, for example shelter inflation in the US, but on the whole the numbers are pointing in the right direction. Recognising this, central banks have started to reduce interest rates, albeit cautiously for now, and the expectation is that they will continue to do so in order to support economic growth. This environment has been positive for bond markets, and also for gold. There are signs of fragility however. Over the last two years there have been multiple occasions where markets have got ahead of themselves by expecting too many interest rate cuts, only to be disappointed when these cuts don’t materialise. For example, coming into 2024 markets expected six rate cuts from the Fed, but we still haven’t had any. We could still be surprised by stronger inflation or economic growth which would delay cuts further which would likely cause a reversal of recent gains in the bond market. The market volatility in August could be seen as a potential red flag. Some parts of the market are clearly stretched, and again this has shown us that the increasing prominence of rules-based trading can exacerbate market moves.

What has been working well for our portfolios, and what has been less effective?

During the rotation in July, our decision to have a relatively low exposure to US technology helped as this sector bore much of the losses. During the volatility in early August, we were shielded from the worst hit areas in the equity market, namely large Japanese companies. Our exposure to bonds and alternatives helped to balance portfolios as these asset classes held up in the face of stock market instability. This was encouraging as we allocate to these asset classes with diversification in mind for such an environment. Our commodity exposure was less effective. Commodities (with the exception of gold) have continued to struggle over the last two months as fears persist over China’s growth outlook, but also on signs that the global economic growth engine may be stuttering. We hold different commodities for different tactical and structural reasons, but if we were to see an upside inflation and growth surprise we would hope this part of the portfolio would perform well.

What is the Committee’s view on Japanese equities, and the Yen?

We continue to hold a constructive view on Japanese equities. We increased our exposure to Japanese equities over a year ago as changes in corporate behaviour and a structural shift to a higher growth and inflation made for positive equity conditions. These conditions have not subsided. We see further upside for company earnings as the domestic economy grows and the global trade cycle strengthens, especially given the market’s outsized weights in pro-cyclical sectors such as industrials, consumer discretionary, technology and financials. Further narrowing of the interest rate differential between Japan and the rest of the world may lead to a stronger yen in the year ahead, and so we hold our equity positions unhedged to benefit from this.

You are continuing to increase your UK government bond exposure at the expense of US government bond exposure, why is this?

The past few weeks have shown us that holding government bonds helps when the market is more concerned with low growth rather than high inflation. We have been adding to government bonds in client portfolios from a very low base as the negative correlation between stocks and bonds has reasserted itself, so these bonds add diversification to portfolios. We are global investors and until earlier this year we were holding predominantly US government bonds. With the market potentially pricing in too many interest rate cuts in the US, we think it is an opportune time to take profits here. We think there could be more cuts than currently expected in the UK, and so are recycling the profits here.

What are your current views on corporate bonds?

Corporates are currently in good health, especially at the large-cap end of the spectrum where the impact of higher interest rates has been more muted. At the margin we are seeing an increase in delayed payments, and even bankruptcies, but our base case is that this won't morph into something more problematic, the current narrow yield spread above government bonds yields isn’t attractive enough to tempt us to allocate more capital here.

There has been much talk of the UK stock market becoming more attractive, you have increased your allocation here, why?

We have marginally increased our UK equity allocation from a low level. This has mostly been in smaller company stocks where current valuations are particularly compelling. We’ve noted that selling pressures in this part of the market have eased following many years of outflows, evidenced by smaller share price falls for companies that miss on earnings over 2024. Expected earnings growth is stronger for this part of the market compared to UK as a whole; driven mostly by sectoral composition differences, but also expectations of falling interest rates having an outsized benefit for smaller companies which typically have more floating rate debt. However, we are being cautious, not least because the employment market for the UK looks to be cooling and sentiment surveys for UK equities are not meaningfully improved.

Manager in focus: Gravis UK Infrastructure Income Fund

Summary

Infrastructure funds invest in public assets and services that are essential for a functioning society, such as power, transport, water and waste. The funds tend to benefit from consistent, long-term returns, low volatility and low correlation to the wider market, making them an attractive addition to a multi asset class portfolio.

Who are Gravis?

Gravis Capital Partners was established in 2008 and became Gravis Capital Management in November 2016. As of August 2024, the group manages £3bn in AUM split between two listed funds and four open ended funds.

Gravis is dedicated to a long-term investment strategy, focusing on assets designed to meet essential needs well into the future. Their distinctive approach includes investments in crucial infrastructure such as hospitals, schools, and student accommodations, all while prioritising environmental, social, and governance (ESG) principles. This strategy also encompasses expansion into key sectors like renewable energy, supported living, logistics, and data centres, setting their fund apart in the investment world and well positioned in our portfolios.

What is the Fund?

The fund is designed to generate income while preserving capital, with the added potential for capital growth. Although it doesn’t track a specific benchmark, the MSCI UK Index is referenced in materials for illustrative purposes. Positioned within the Investment Association Infrastructure Sector, the fund currently holds assets totalling £632 million and targets a yield of 5% per year, net of fees.

The fund primarily invests in GBP-denominated equities, mainly those listed in the UK and involved in the broader infrastructure sector. Alongside equities, the fund may also include other investments such as bonds, collective investment schemes, money market instruments, deposits, and cash. With a specific focus on Sterling assets, the fund prioritises investments centred in the UK but does not limit itself to any particular geographical area, industry, or economic sector beyond this focus.

Investment Philosophy

Gravis specialises in infrastructure and real estate investments, focusing on a long-term strategy to deliver stable and predictable returns. Their approach is to invest in companies with sustainable business models and reliable, long-term cash flows, which help ensure consistent returns. The primary goals are to preserve capital, provide regular income, and minimise volatility.

As active managers, Gravis carefully monitors factors like yield sustainability, inflation protection, valuations, liquidity, and volatility. They strive to generate diversified, stable, risk-adjusted returns while keeping costs low.

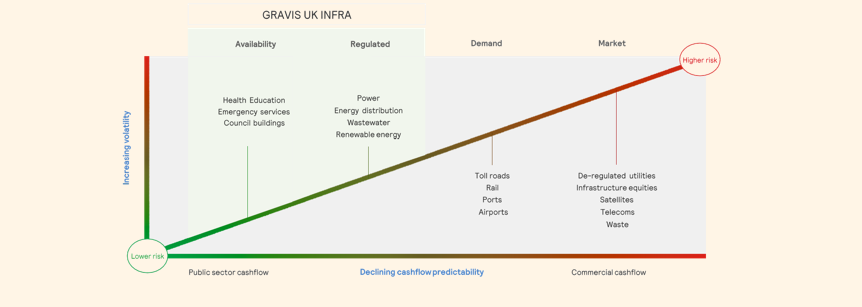

The chart below illustrates how Gravis’ investment philosophy emphasises cash flow predictability while minimising volatility. With a preference for “Core” infrastructure assets, the fund focuses on stable, public-sector, inflation-linked cash flows, resulting in lower volatility of returns.

The investment universe is made up of listed, GBP denominated securities within the broad infrastructure sector. This includes investment trusts, REITs, equities, and fixed income. Currently, 78% of the fund is in investment trusts, with the balance in direct equities or cash. The top 10 holdings are all investment trusts.

There are two main types of assets that the team focuses on:

- Demand-based projects, such as toll roads, which generate revenue based on number of users.

- Availability-based assets, such as hospitals, which receive revenue through guaranteed payments which are often backed by the UK government, and regardless of usage levels.

Blending these two types of income bearing assets offers a compelling, highly inflation protected, and resilient portfolio that is less geared to the economic cycle. Another key benefit is higher certainty around revenue and profitability, provided by availability-based assets, mixed with higher income generating assets, from demand-based investments.

Performance

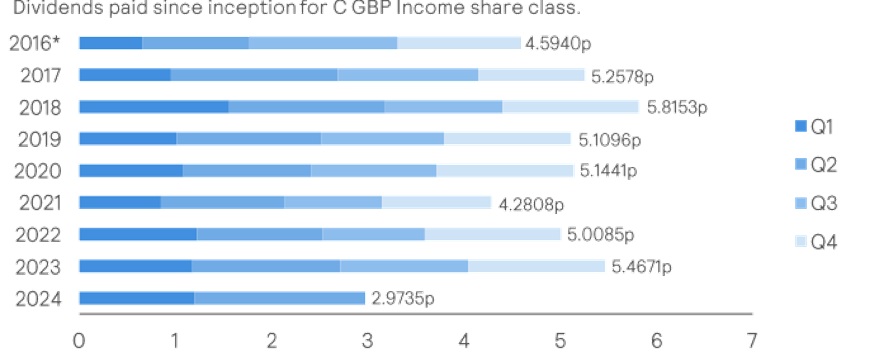

- The main focus in terms of fund performance is to generate income of around 5% per annum.

- Below I have highlighted the dividend returned to investors each year since 2016.

- Furthermore, the fund has delivered a 32% return on investment since 2016 through capital appreciation.

ESG

Gravis has been committed to responsible investment practices since January 2019, when it became a signatory to the Principles for Responsible Investment (PRI). This commitment was further strengthened in February 2022, when Gravis joined the UN Global Compact Network, aligning its operations with principles focused on human rights, labour standards, environmental sustainability, and anti-corruption.

Gravis is also dedicated to following the recommendations of the Taskforce for Climate-related Financial Disclosures (TCFD), actively working to identify and address climate-related risks and opportunities within its portfolio.

In 2021, Gravis implemented a formal Voting and Engagement Policy, aiming to vote on all holdings at every meeting. Their voting process is systematic, guided by ISS research and aligned with ISS Sustainability Proxy Voting Guidelines.

Saltus Investment Case

Will Argent (Portfolio Manager) is an experienced manager, with a good track record, and the backing of a reputable infrastructure boutique in the form of Gravis. His offering is sensibly managed, has broad exposure to UK core and renewable infrastructure assets, which is almost wholly accessed through the investment trust structure.

The fund is differentiated in that it has a UK focus, which immediately significantly narrows down the pool of available funds, and within this small pool, it has consistently outperformed its direct peers on both an absolute and risk adjusted basis.

Gravis is committed to responsible investment, being a signatory to the PRI since 2019, joining the UN Global Compact in 2022, adhering to TCFD recommendations, and implementing a formal Voting and Engagement Policy guided by ISS Sustainability Proxy Voting Guidelines.

Saltus use this fund as part of a diversified portfolio. This is not a recommendation to invest in this fund. Saltus will not be liable for any losses incurred as a result of investing in this fund.

Asset Allocation Committee

The committee consists of several senior members of the investment team, all partners, who invest their own money alongside clients. The committee is led by:

David Cooke

Co-Chief Investment Officer , Saltus Asset Management Team