Investment conditions

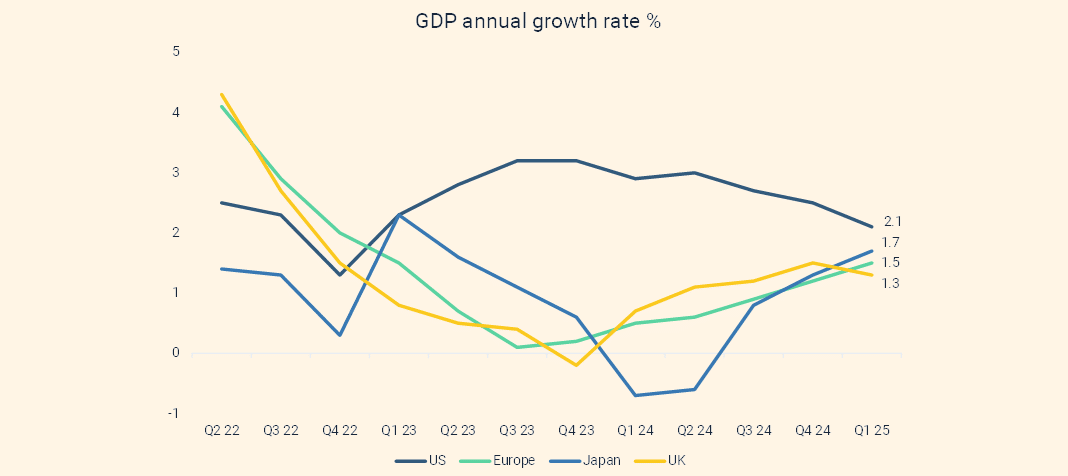

The global economy continues to grow at a healthy pace. First quarter GDP growth remained in positive territory on a year-on-year basis, but as the US economy continues to slow, Japan, Europe and UK growth rates remain on their upward trajectory. These readings came before Trump’s trade wars were announced, so there is more uncertainty around GDP growth from here, and forecast growth rates have been revised down but not into recessionary territory yet. The second quarter GDP growth data should start to show any tariff-related impact.

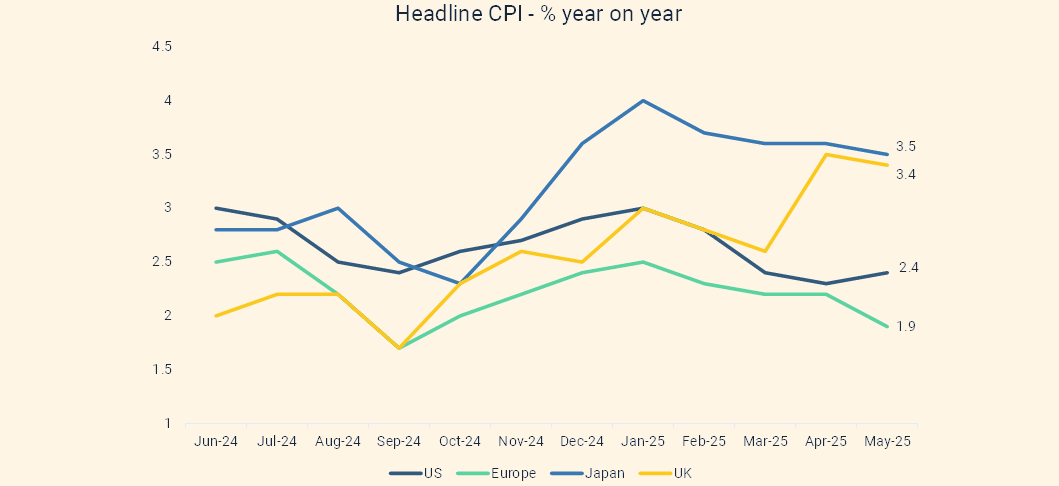

Although there was a slight tick up in headline US inflation from April to May, it currently stands at 2.4%. In Europe, inflation has fallen below the central bank’s 2% target. Whilst in the UK and Japan, inflation is still considerably higher than the 2% target. Services inflation is still relatively high in most regions, and wages continue to rise, highlighting the stickiness of inflation. Central bank speakers have been signalling that they are waiting to see if tariffs have a meaningful impact on inflation, and that this is making them proceed with caution on rate cuts. The May inflation data showed no discernible tariff impact, but this could be due to front-loading of exports before the tariffs came into place. China has experienced deflation for the last four months.

Source: Saltus, Trading Economics

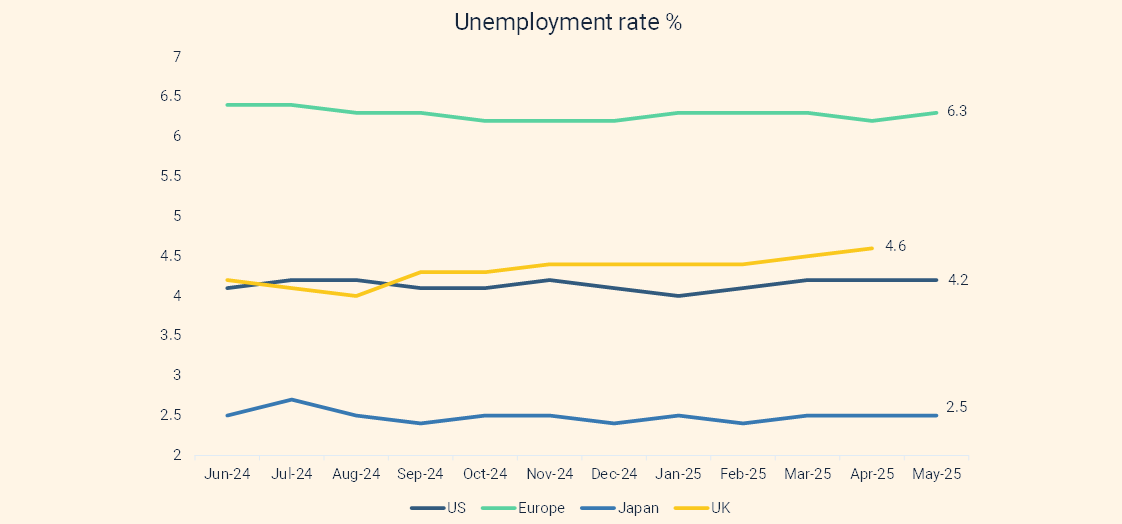

Unemployment is still near historic lows in the developed economies. This is supporting healthy wage growth, which is bolstering the consumer. A buoyant consumer has been a key pillar of economic growth and earnings growth in this cycle.

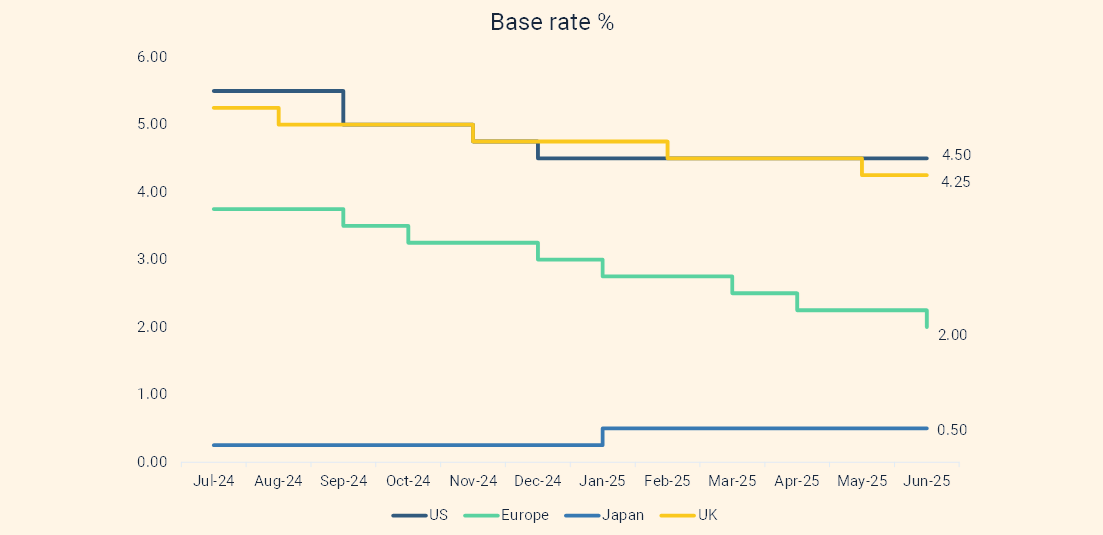

The only central bank action of note during the period was an eighth interest rate cut from the ECB in their June meeting, accompanied by commentary that they would likely pause their cutting cycle for now. The Fed, Bank of England and Bank of Japan all held rates steady, citing resilient economic growth, acquiescent inflation, and tariff uncertainty. The Bank of England signalled they will likely cut at their next meeting in August, and Fed rate setters remain divided on the timing of the next cut.

Source: Saltus, Trading Economics

Amid the tariff-induced volatility in financial markets, first quarter corporate earnings season was solid. Companies globally showed signs of strength ahead of a surge in global trade tensions, however many companies offered cautious guidance around the potential impact of tariffs. Earnings globally rose 6.5% from the same quarter one year ago, while sales rose 3.2%. As earnings grew more than sales, this means that profit margins expanded over the past 12 months. Looking forward, analysts expect 8.8% earnings growth for global equities over 2025. Regionally, Emerging Markets earnings are forecast to grow quickest at almost 19%, whilst the UK, Japan and Europe have more subdued forecasts at -0.2%, 1.4%, and 3.9% respectively. These regions all trade cheaper than their long-term averages on a price to earnings multiple, whereas the US remains overvalued.

Market Themes

Emerging Defiant

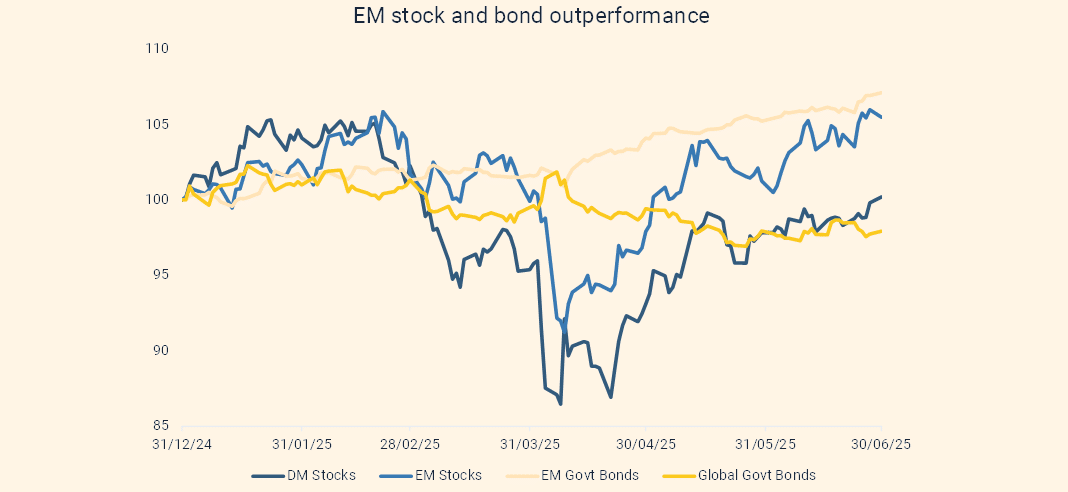

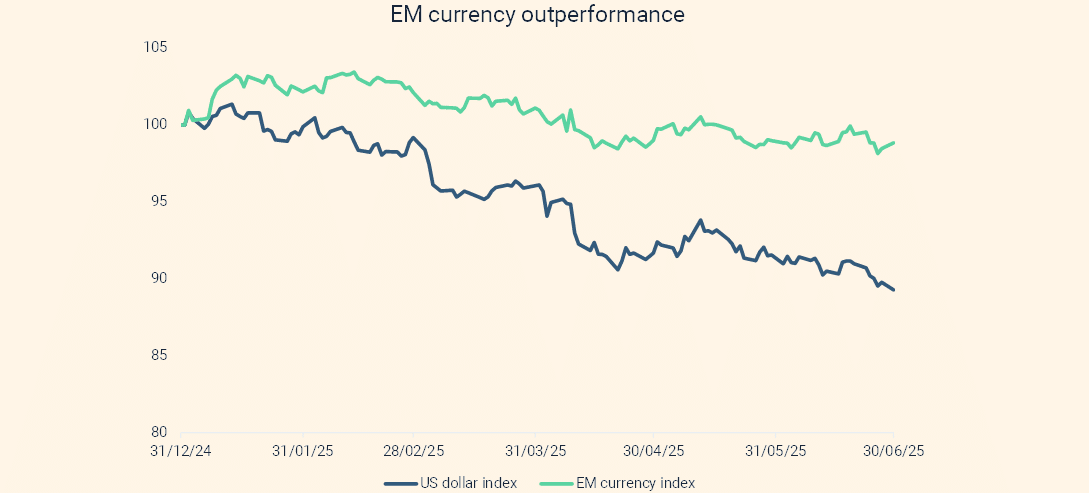

When Donald Trump started waging trade war, an investor could’ve been forgiven for thinking that emerging markets would suffer as a result. With China and Mexico in the crosshairs, and many Asian countries targeted for their large trade surpluses with the US, it seemed emerging market assets were in danger. We have seen the opposite though, with stocks, bonds and currencies in these regions outperforming their developed world counterparts.

Part of this has been due to a need for investors to diversify out of US assets due to Trump’s unpredictable policies, as explored in this article (2025: The story so far… | Saltus). But this strength is also due to attractive prospects for emerging market economies, monetary policy, and corporate earnings. At the end of June 2025, a Bloomberg index of local currency bonds of large emerging markets, and an MSCI gauge of their shares have gained 5% and 7% in 2025 to date respectively. In comparison, the MSCI World index and the FTSE World Government Bond index are flat to down for the year.

A weakening dollar has been a tailwind for emerging markets as it relieves pressure on their own currencies, reduces the value of their USD-denominated debt, and gives central banks more room to loosen monetary policy which supports economic growth and markets. Interest rates and bond yields are still relatively high, making emerging market bonds attractive, and in a number of regions there aren’t the same debt sustainability worries that haunt a number of fiscally profligate developed countries. As mentioned above, corporate earnings estimates are the highest for any region for 2025.

For these reasons, we continue to hold an overweight position in emerging market equities, and an allocation to emerging market debt.

Source: Saltus, Bloomberg (100 = 31/12/24). DM Stocks = MSCI World, EM Stocks = MSCI EM Index, EM Govt Bonds = Bloomberg EM Local Currency Government Index, Global Govt Bonds = FTSE World Government Bond Index, EM currency index = JPMorgan EM Currency Index

The Long End

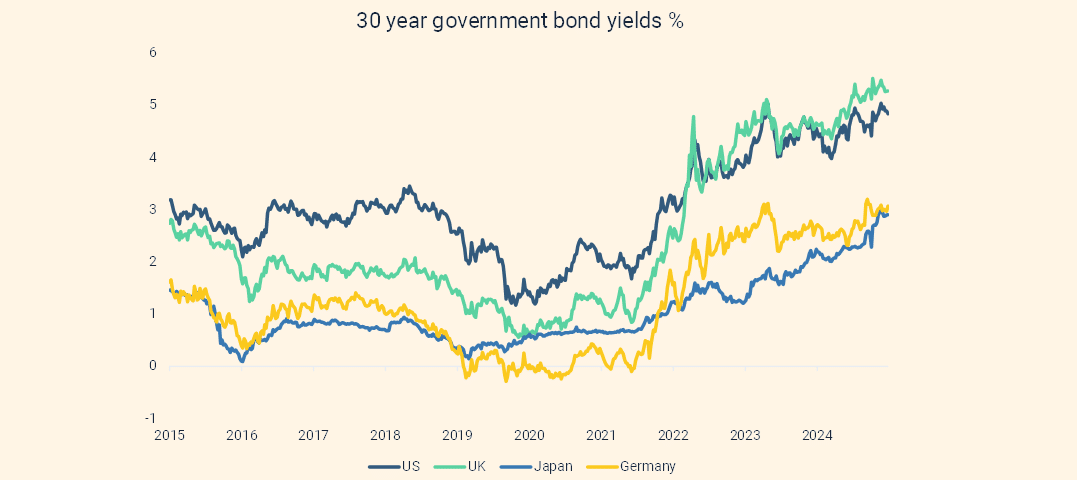

Long-dated bonds have been feeling the pressure recently. In developed economies, long bond (30 year maturity) yields have spiked higher. Investors are reconsidering their willingness to lend for the very long term to governments in advanced economies.

In Japan, the moves have been most striking as inflation has returned after many decades, and there has been a decline in demand from traditional domestic buyers. This rise got so extreme at one point, the authorities had to step in to steady the market.

In the US, Trump’s One Big Beautiful Bill Act, which is in consideration, is expected to add trillions of dollars to the US debt pile over the next decade. This has resulted in a swift exodus of investors from US bonds.

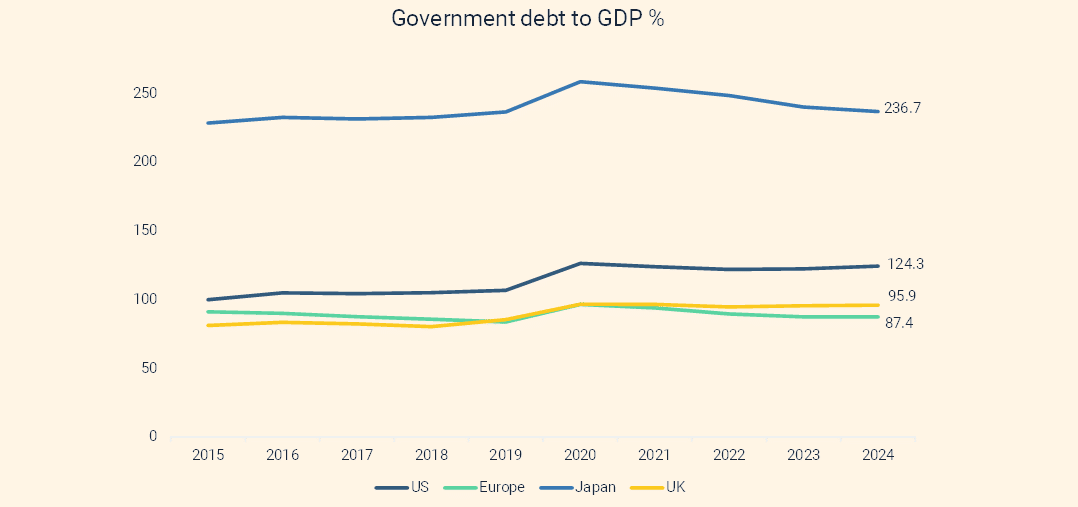

The UK has well known problems in the long end of the gilt market, which were brutally exposed three years ago. There are nerves surrounding the current government’s spending plans, and methods to fund these, and the government is finding it hard to reign in the debt load.

These fiscal jitters are coinciding with a period of higher inflation, and a period where governments are making bold spending commitments on defence and infrastructure, which will only add fuel to the inflationary fire. On top of this, as bond yields rise, governments have to spend more on servicing the interest on their debt, rubbing salt into the wound.

At the moment, these losses have been contained to the long end of the yield curve, however if the pain starts spreading to other parts of the bond market, this could bleed through into other asset classes, as we saw in 2022. It is an area of the market we are monitoring closely, and it is why we are avoiding long duration bonds, and US government bonds on the whole.

Source: Saltus, Bloomberg, Trading Economics

Views by asset class

Equities

Since the last Asset Allocation Committee meeting in April, equity markets have been remarkably sanguine. Much of this optimism is based on the hope that tariffs won’t be anywhere near as high as they were signposted to be on ‘Liberation Day’ on 2 April 2025. Through May and June, stock markets recovered all of their losses, and once again sit near all-time highs, barely blinking when war broke out in the Middle East in late-June.

Markets have now had sight of April, May and indicative June economic and inflation data, and so far it is difficult to see any material tariff-related impact here. Even on the corporate side, there has been little evidence of lower profit margins, or price increases.

Solid data, combined with a belief that tariffs won’t be as severe as initially expected has kept the stock market momentum positive. We continue to have a ‘glass half full’ stance on equities therefore, whilst maintaining our balance between US equities, and Rest of World equities. Non-US regions that we favour are Emerging Markets (see section above), Europe (2025: The story so far… | Saltus), Japan and the UK. We initially started allocating to these regions given attractive valuations on offer, but over the last 6-12 months we have increasingly become worried about the backdrop for US equities, and have traded accordingly.

At the most recent meeting, the committee decided to increase our exposure to Japanese equities. This is an overweight position we have held for a while now for reasons mentioned here (Japan’s Economic Renaissance). We are bolstering our exposure here now given that Japanese equities have de-rated over the past 12 months, which is counter to most other regions, leaving them cheap versus global equities. We still believe there are positive tailwinds to the market coming from improving corporate governance and shareholder returns (buybacks), increasing investor activism, improving profitability, increasing interest from foreign investors, and an economic turnaround resulting in higher wages. A tariff resolution would be a boon for the market too.

Apart from this addition, no other major changes to the equity book were decided upon. This is a reflection of the fairly significant changes we have made over the last 6 months, and the fact that we are comfortable with our positioning going forward from here.

Bonds

Although government bond yields look relatively attractive, the committee are still cautious about the outlook for inflation, economic growth and interest rates, especially in the US. This is combined with concerns over government debt levels and spending commitments (see section above). We continue to favour short to medium maturity, ex-US government bonds – primarily UK and European government bonds – as we believe there is more scope for interest rate cuts, lower inflation, and lower economic growth. Where we do have US government bond exposure, this is through inflation-protected bonds, given concerns around sticky inflation.

Within corporate bonds, we are maintaining a high quality tilt towards investment grade, with shorter duration given the lower risk in this part of the bond market. Credit spreads continue to tighten, and don’t seem to be reflecting an increased risk of a tariff-induced economic slowdown.

We maintain our exposure to high yield corporate bonds as a risk-on position rather than a defensive position, replacing equity exposure. The same goes for our exposure to emerging market debt.

Alternatives and Currency

The committee recently took the decision to sell part of our gold miners position. These positions have been a large contributor to positive performance so far in 2025 as gold mining shares have outperformed a strengthening gold price, and have seen returns in excess of 60% in the year to date. The committee decided it was prudent to bank some profits on these positions, in the event of a turn down in stock markets, or a turn down in the gold price. We are holding the proceeds in cash for now as we look to re-enter on any weakness, or if we find another similarly attractive investment opportunity. We are maintaining a position both in gold mining shares, and physical gold, as we believe there is more upside in both given that central banks and investors are buying more gold, in order to diversify out of US dollars. We think gold offers effective portfolio diversification benefits given it has been performing positively in the face of heightened volatility.

Elsewhere in the alternatives space, the committee discussed initiating a position in copper. The committee are still positive on the long-term supply/demand mismatch in the copper market, but decided to wait for a potentially better entry point once there is more clarity on US copper tariffs, and global reciprocal tariffs which could create short term volatility in the copper price.

We maintain an overweight position in macro hedge, absolute return, and equity long/short strategies. These are important diversifiers in the portfolio and tend to perform relatively well in more volatile markets, providing ballast to the rest of the portfolio. These positions held up well during the turbulence in April, and meant our portfolios weren’t as affected as broader markets.

The committee left currency weightings unchanged. Our US dollar exposure has fallen naturally as we have reduced our exposure to US assets. We still hold an active position in the Japanese yen given its tendency to strengthen in falling markets, again providing portfolio ballast in the face of higher volatility.

Summary of positioning

Below is a summary of our views for each asset class, from strongly negative (- -) to strongly positive (+ +).

Asset Class

| Asset class | -- | - | Neutral | + | ++ |

|---|---|---|---|---|---|

| Equities | X | ||||

| Government bonds | X | ||||

| Corporate bonds | X | ||||

| Alternatives | X | ||||

| Cash | X |

Asset Class Breakdown

| -- | - | Neutral | + | ++ | ||

|---|---|---|---|---|---|---|

| Equities | USA | X | ||||

| UK | X | |||||

| Europe | X | |||||

| Japan | X | |||||

| Asia ex-Japan | X | |||||

| Emerging markets | X | |||||

| Bonds | US Government | X | Non-US Government | X | ||

| Inflation-Linked Government | X | |||||

| Investment Grade Corporate | X | |||||

| High Yield Corporate | X | |||||

| Emerging Market Debt | X | |||||

| Alternatives | Commodities | X | ||||

| Gold & Gold Miners | X | |||||

| Property | X | |||||

| Global Macro | X | |||||

| Equity Long/Short | X | |||||

| Absolute Return | X | |||||

| Infastructure | X | |||||

| Currency | Sterling | X | ||||

| US Dollar | X | |||||

| Euro | X | |||||

| Japanese Yen | X | |||||

| Emerging Markets | X |

Fund in focus: Janus Henderson European Smaller Companies

Summary

This is a well-managed European smaller companies fund that invests across all stages of a company’s lifecycle, from early growth to maturity, providing broad exposure to compelling investment opportunities.

The team is led by experienced portfolio managers with a proven ability to consistently generate return, particularly within the smaller-cap segment of the market where specialist expertise is essential.

The fund focuses on quality growth stocks trading at reasonable valuations, consciously avoiding overexposure to early-stage, higher-risk, high-growth names often associated with this part of the market.

Janus Henderson and the team

Janus Henderson is a well-established, global asset manager with over $200 billion in assets under management and a team of more than 340 investment professionals worldwide. The firm was created in 2017 through the merger of two complementary businesses with deep, independent histories. Henderson Global Investors, founded in the UK in 1934, was known for its bottom-up, research-driven investment strategies. Janus Capital Group, established in the US in 1969, also had a strong focus on fundamental, analysis-led security selection. Together, their merger brought together regional expertise to create a truly global investment platform.

The fund is co-managed by Ollie Beckett and Rory Stokes, who bring significant experience and a strong track record in European smaller companies. They are directly supported by Julia Scheufler, who has worked closely with the managers since 2018, providing valuable research and portfolio support. The team also benefits from the depth and breadth of the wider Janus Henderson European equities team, which includes 10 additional portfolio managers and analysts. They regularly collaborate with Janus Henderson’s UK Smaller Companies team and draw on the firm’s dedicated ESG specialists and a global trading desk of 35 dealers, ensuring efficient execution and strong environmental, social, and governance integration across the investment process.

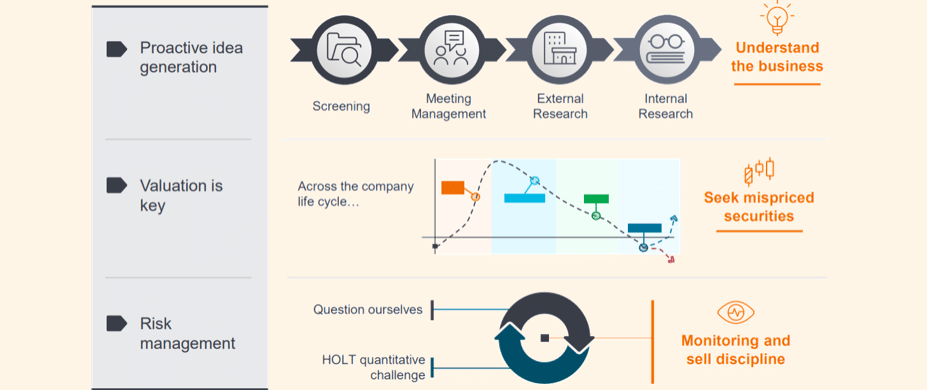

Investment Philosophy

At the heart of the fund is a bottom-up stock-picking approach, where the focus is firmly on identifying individual companies with the potential to consistently outperform the market. The managers look for clear, long-term trends that drive success and aim to invest in businesses that exhibit these qualities, typically companies with strong competitive positions, pricing power, and attractive long-term growth prospects. A particular emphasis is placed on finding businesses with sustainable, durable cash flows, which the team believes are key to delivering reliable long-term returns aligning with our Saltus top-down strategic view.

The fund’s investment philosophy is built around three core principles:

- Research-led idea generation: A bottom-up, fundamental approach driven by detailed management due diligence, deep market knowledge, and rigorous research.

- In-depth company valuation: Actively investing in companies at different stages of their business journey, with the aim of balancing value and growth opportunities across the portfolio.

- Proactive risk management: Consistent analysis and testing to ensure that companies maintain alignment with the investment philosophy.

Source: Janus Henderson

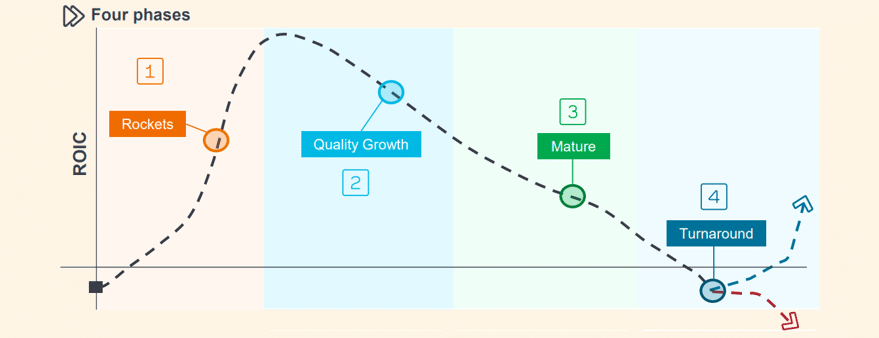

To capture these life-cycle stages, the portfolio is divided into four distinct categories:

- Quality Growth: Established companies with strong competitive advantages and steady growth.

- Rocket: High-growth businesses with rapid expansion potential.

- Mature: Solid, stable companies offering value and dependable cash flows.

- Turnaround: Companies undergoing significant positive change, offering potential for recovery and re-rating.

Source: Janus Henderson. * ROIC = Return on Invested Capital

These categories allow the managers to build a well-diversified, dynamic portfolio that can adapt over time. The balance between each category naturally shifts based on where we are in the business cycle and where the managers see the best opportunities from a valuation and growth perspective.

Performance

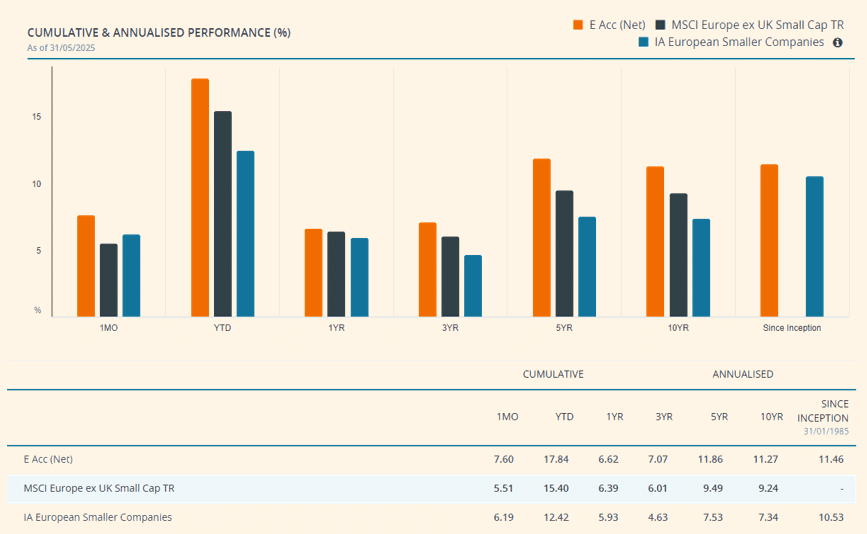

The fund has delivered exceptional performance, consistently outperforming both the MSCI Europe Index and the IA European Smaller Companies sector benchmarks. Since its inception, the fund has achieved an impressive annualised gross return of 11.5%, highlighting the strength of the team’s stock selection and disciplined investment approach.

So far this year (as of 31 May 2025), the fund has posted a strong year-to-date return of 17.9%, further reinforcing its ability to capture market opportunities.

Looking at the longer-term picture, the fund’s track record is even more compelling. It has demonstrated a consistent ability to deliver excess returns in rising markets while effectively managing downside risks during more challenging periods, a hallmark of the managers’ balanced, research-driven approach.

Source: Janus Henderson

Saltus rationale

This is a well-managed European smaller companies fund that invests across all stages of a company’s lifecycle, from early growth to maturity, providing broad exposure to compelling investment opportunities.

The team is led by experienced portfolio managers with a proven ability to consistently generate return, particularly within the smaller-cap segment of the market where specialist expertise is essential.

The fund focuses on quality growth stocks trading at reasonable valuations, consciously avoiding overexposure to early-stage, higher-risk, high-growth names often associated with this part of the market.

The fund has demonstrated strong upside participation while managing downside risk effectively, consistently delivering outperformance against its peer group over the long term.

Performance is primarily driven by the managers’ disciplined stock selection and adherence to a clear, core investment style, rather than relying on market trends or sector bets.

Saltus use this fund as part of a diversified portfolio. This is not a recommendation to invest in this fund. Saltus will not be liable for any losses incurred as a result of investing in this fund. Past performance is not a reliable indicator of future results.

Asset Allocation Committee

The committee consists of several senior members of the investment team, all partners, who invest their own money alongside clients. The committee consists of:

Charles Ambler

Co-Chief Investment Officer, Saltus Asset Management Team

David Cooke

Co-Chief Investment Officer , Saltus Asset Management Team

Andy Cawker

Chairman of the board of Saltus Partners LLP and Saltus Asset Management, Saltus Asset Management Team

Joshua Biele

Investment Analyst, Saltus Asset Management Team

Tom Harrison

Investment Analyst, Saltus Asset Management Team

Clive Martin

Financial Planner, Saltus Asset Management Team