Investment conditions

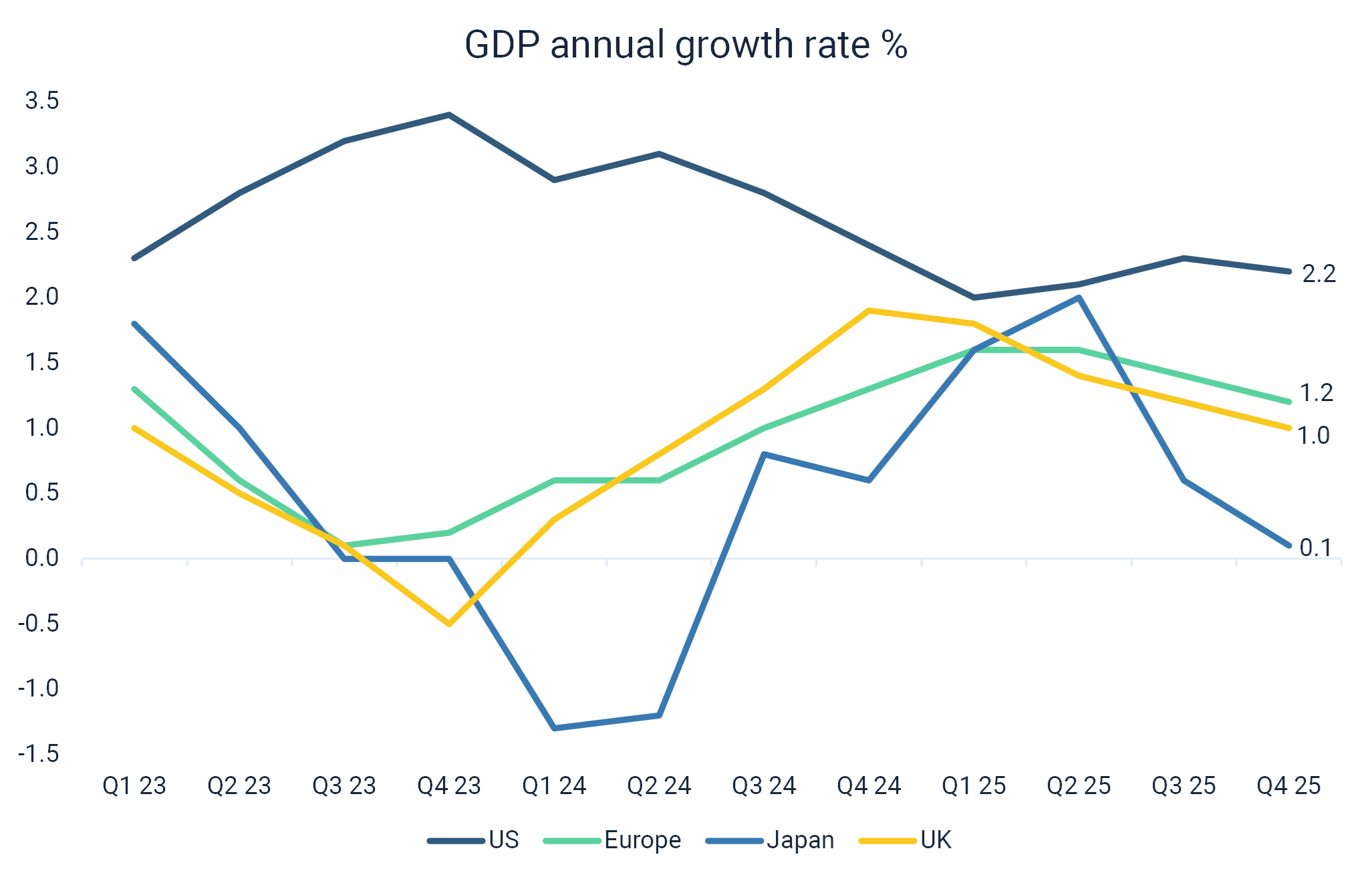

Broad economic growth eased towards the end of 2025, although it remains at healthy levels with positive momentum. The outlook remains for growth in 2026 to be at or above trend, supported primarily by continued strength in the United States. The US economy is still benefitting from vast amounts of AI capital expenditure, falling interest rates and low unemployment, which could help offset the geopolitical turbulence emanating from the US.[1] A prolonged oil price rise could reduce economic growth through 2026 if we see significant supply disruptions.[2] Europe, UK and Japan are more exposed to rising energy prices as they are large energy importers.

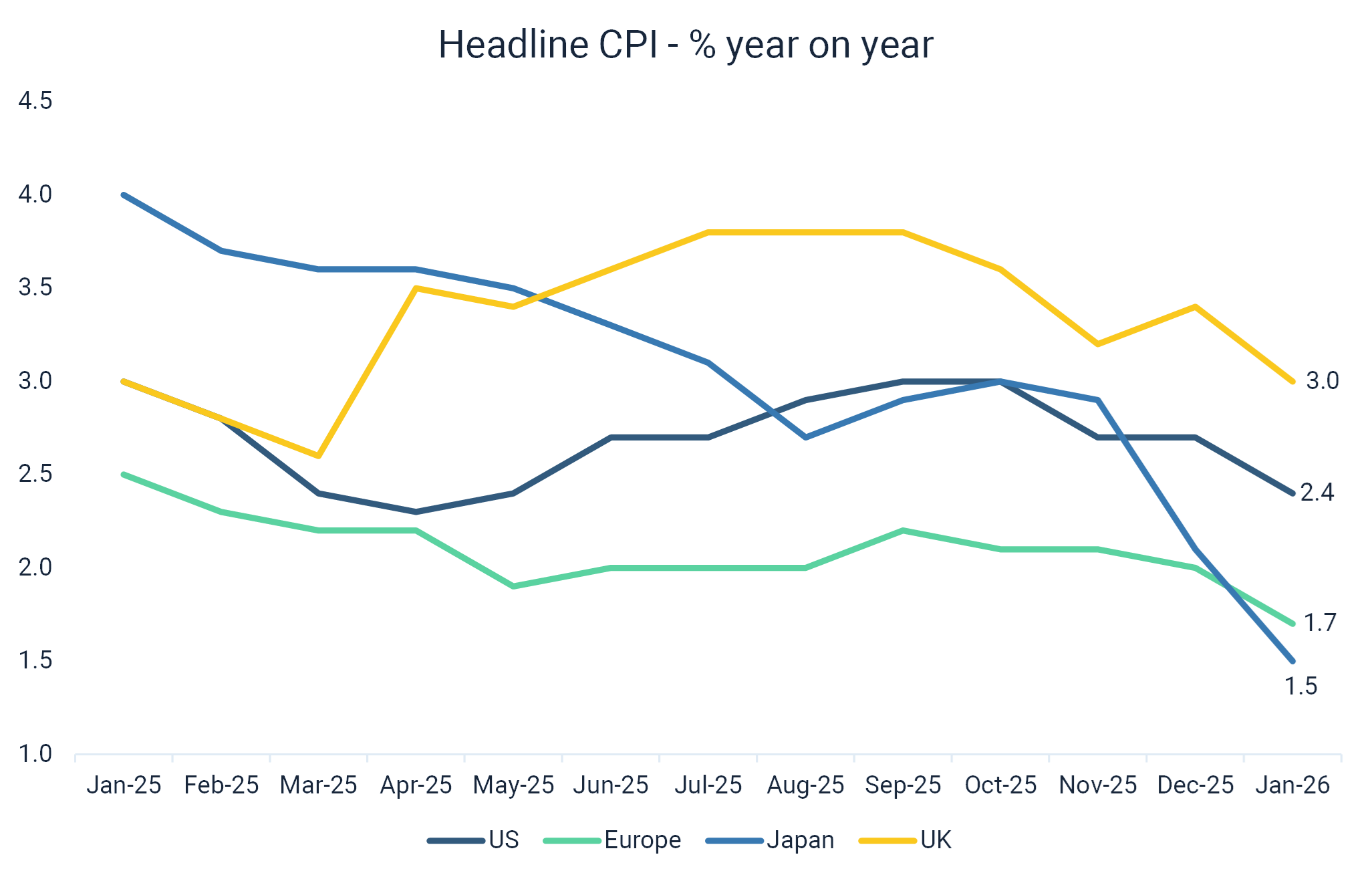

Inflation continues to fall and is now almost in line with central bank targets. The exception to this is in the UK, where inflation, even though it has fallen, is still significantly above the Bank of England’s target. [3] The increase in US tariffs has not had a meaningful impact on inflation in the US, however, a prolonged oil price shock could cause inflation in all regions to start picking back up, akin to 2022 when Russia invaded Ukraine.

Source: Saltus, Trading Economics

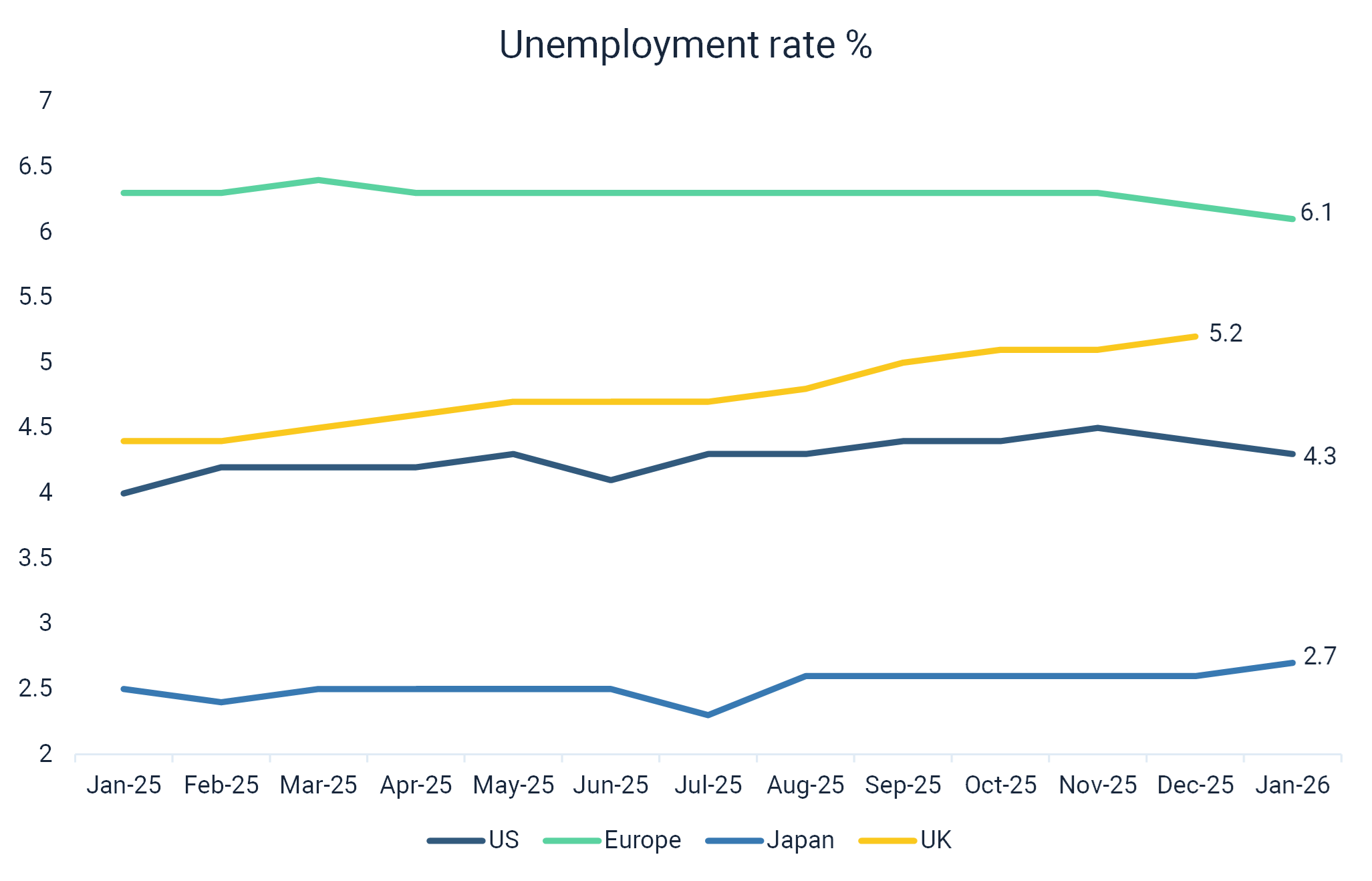

Unemployment across the major economies remains near record lows. This is supporting healthy wage growth, which is bolstering the consumer. A buoyant consumer has been a key pillar of economic growth and earnings growth in this cycle. The US labour market looks like it is slowing down though, and this is a closely watched indicator to signal if the US economy is going to experience a protracted economic slowdown. The UK labour market looks weak, due to many of the growth-negative tax rises that have taken place over the last year.

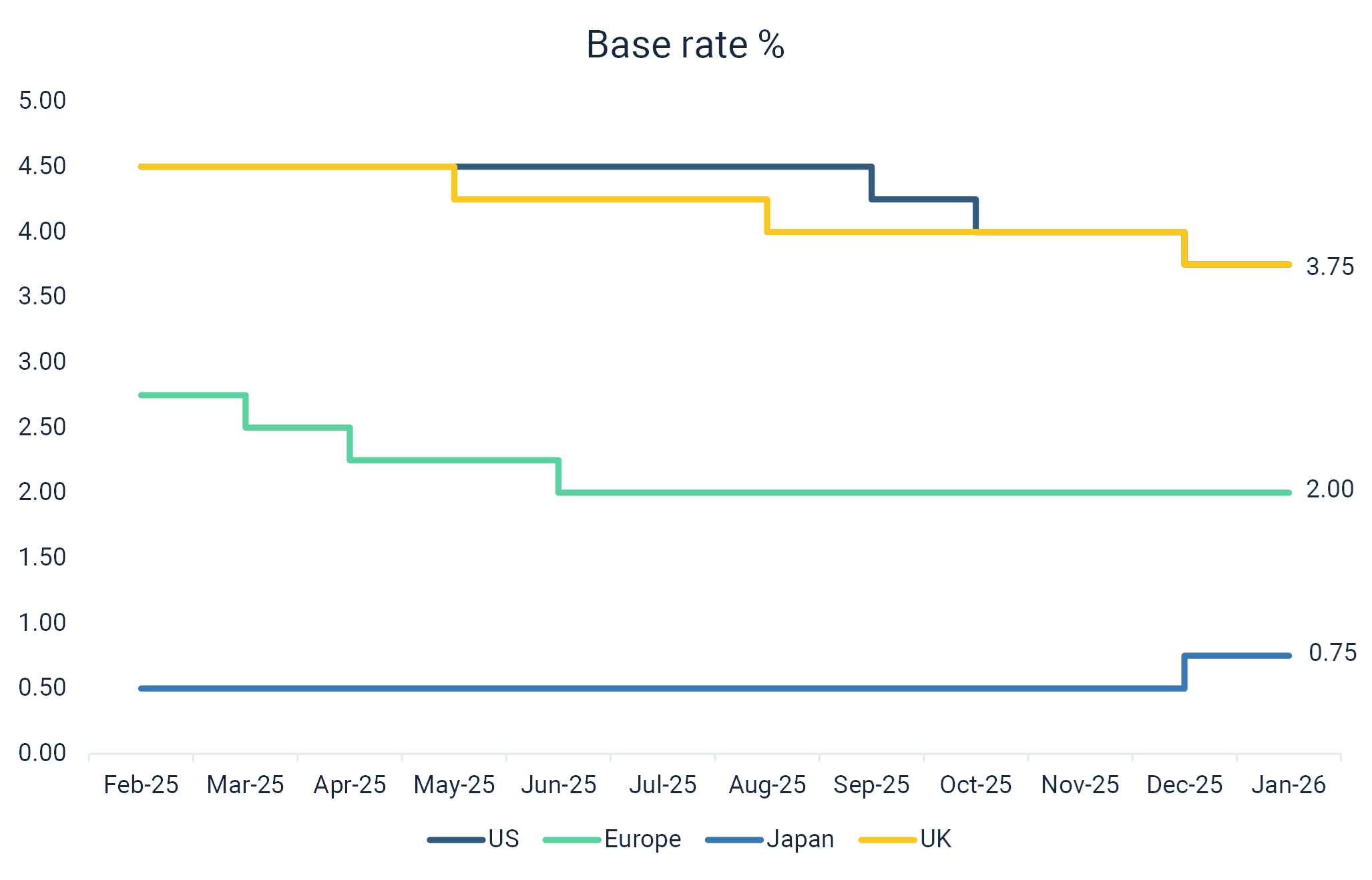

There were no notable interest rate changes in the last two months. Rising inflation expectations caused by a spike in the oil price have caused markets to reduce their expectation of any further rate cuts in the US and UK this year. The Bank of Japan are expected to continue hiking, albeit slowly, and the European Central Bank could hike rates towards the end of 2026. The cutting cycle could be over for now.

Source: Saltus, Trading Economics

Fourth quarter corporate earnings results were robust. Corporates are still in a healthy position given resilient economies, positive consumers and rising wages. US technology companies were strong, but there was more dispersion between companies during this quarter, with the market starting to tire of the huge capital expenditure announcements. Looking forward, analysts expect healthy 19.6% earnings growth for global equities over the next 12 months. Regionally, Emerging Market earnings are forecast to grow quickest over the next 12 months, at 39.9%, with Asia ex-Japan corporate earnings also forecast to grow strongly at 38.9%. The UK and Europe have more subdued forecasts at 9.5%, and 11% respectively, but across the board the expectation is that 2026 will be another strong year for corporates. All regions are trading in line with their long term averages on a price to earnings multiple, except Emerging Markets and Asia ex-Japan which are trading slightly below. This consensus earnings and valuation data is taken from Bloomberg.

Market Themes

Dominating both financial and non-financial headlines is the conflict between Israel/US/Iran and the consequences for the energy market. We have discussed this in detail here Middle East conflict – market update | Saltus and we continue to monitor any impact on markets daily.

Below are a couple of other interesting market themes.

AI scare trade

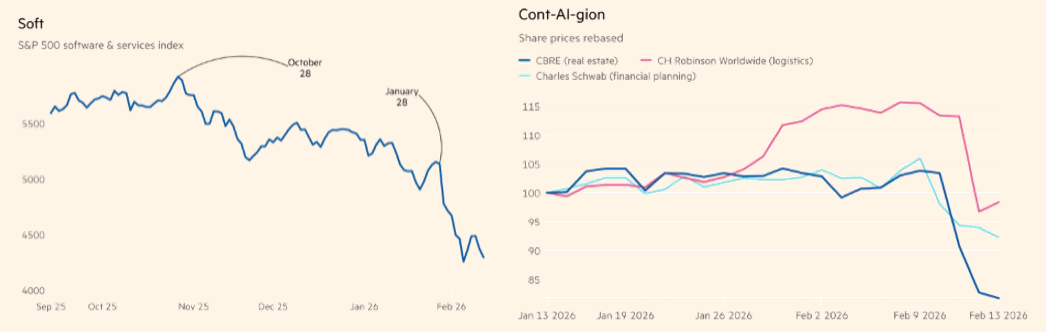

Since mid-February, stock market sectors perceived to be vulnerable to AI-driven disruption have aggressively sold off.[4] This has been characterised as ‘sell now, ask-later’ investor behaviour, as rather than pick winners and losers, investors are indiscriminately selling their positions in the affected sectors.

The first sector to feel the wrath of the AI scare trade was software, in what is being touted as the ‘SaaS-pocalypse’.[5] Given the advances in AI tools that can write code, serious concerns have been raised over the core subscription models and pricing power of software companies. Popular stocks and indices in the sector have fallen between 20% – 30%, as investors work through the impact on individual companies’ business models from the new tools. This is made more difficult as more AI productivity tools are released each week.

What started in the software sector has spread to Wealth Management, as new AI-enabled tax and financial planning tools have been released. These are seen as providing routine tax and planning optimisation strategies more cheaply. Since then, Logistics, Cybersecurity, Consulting, Education, Property and Insurance have all been in the AI Scare Trade’s crosshairs. The market’s attention has shifted from the potential upside of AI tool providers to the impacted end users. There is a general feeling of negative sentiment around AI, and whilst these sectors have felt the blunt force of investor panic, it will be a while before businesses and investors have a clearer picture of which business will fail, and which will flourish as a result of these new technologies.

Source: LSEG via markets.ft.com

Private credit woes

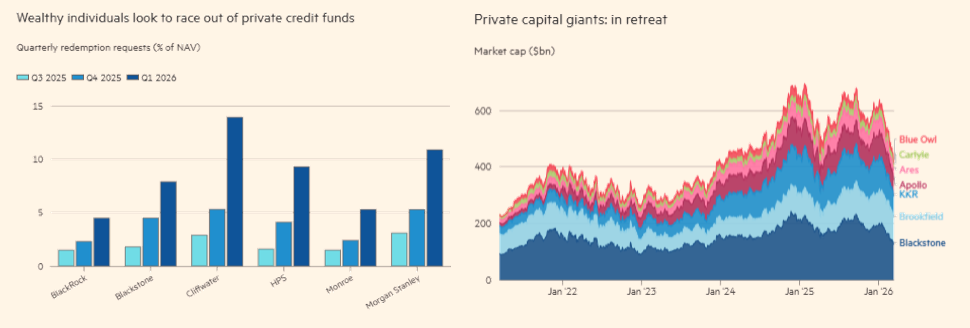

When two US companies, First Brands and Tricolor, filed for bankruptcy in 2025, alarm bells rang in the private credit sector as these companies had raised large sums of money through private borrowing. Huge amounts of capital have flowed into this asset class in the last few years as companies eschew traditional bank lending and the public bond markets (and all the inconvenient scrutiny that goes with them) and raise money from private lenders instead. The lenders in theory lend at a higher interest rate, with less frequent pricing of their assets, a feature that made private equity so attractive.

The alarm bells have grown louder so far in 2026. A significant proportion of private lending goes to software companies, which as mentioned above, aren’t in the market’s favour currently. This has led to increased redemption requests from investors, and in some cases, large private credit funds have been ‘gated’, where investor redemptions are restricted. Talk of gating brings back memories of property funds in 2007, and so more investors have run for the exit. Given the illiquid nature of the asset class, this in turn leads to more gating.

This is more acute in the private credit funds targeting retail investors, as these funds have typically been offered as ‘semi-liquid’, resulting in an even more extreme liquidity mismatch. Big names like BlackRock, Morgan Stanley, Blackstone and Blue Owl have all been affected.

Currently, whilst the economy is strong, interest rates are coming down, and AI has yet to cause widespread business failure, it is unlikely a credit crisis is afoot. This is more likely a liquidity mismatch between what retail investors need, and how the asset class is designed. If we are experiencing these issues at a time of limited credit stress, it is worrying to think of the liquidity issues if there is a real downturn in the credit cycle and more defaults start coming through.

Views by asset class

Equities

The committee decided to maintain the current regional equity exposures. Around half our equity exposure is in the US, which we consider to be underweight given the US dominance in the global stock market. The other half of our equity exposure is spread broadly, with notable positions in emerging and frontier markets, and Japan.

Within our US exposure, for the last two years we have purposefully sought to diversify away from the technology sector given valuation concerns, concentration concerns, and too much dependence on the AI narrative. At the recent meeting the committee decided to reduce our underweight to the US technology sector, but whilst still remaining under exposed. In the last four or five months, there has been a meaningful rotation away from technology and into the broader US stock market, which has benefited our positioning. The valuation premium of the technology sector has reduced, whilst the earnings outlook for the sector remains robust. The committee believes this provides a good opportunity to reduce our underweight position.

The committee also decided to alter the composition of our emerging and frontier market exposure. We are increasing our exposure to the emerging market index, and funding this from our active positions. The emerging market index has a significant allocation to Korea, Taiwan and China technology. These markets have suffered heavily in the past few weeks since the outbreak of conflict in the Middle East, presenting a good entry point to start building a position here.

The committee reviewed our exposure to Japan, Europe and the UK in light of current events, and were happy to leave these positions unchanged for now. The conflict in the Middle East is an ever-changing and fast moving picture. We are well positioned to move swiftly if required.

Bond

Within our fixed income exposure, we currently do not have a meaningful position in government bonds due to concerns around lingering inflation, fewer rate cuts, and the debt burden of developed economies. Where we do have government bond exposure, this is predominantly in UK gilts with a small holding in US inflation-linked bonds. The committee decided to reduce our exposure to the long end of the UK gilt market, reducing interest rate sensitivity. The long end of the UK gilt market has been strong recently, and we are concerned about the high level of correlation at the long end of government bond markets globally.

Within corporate bonds, we had exposure to both investment grade and high yield debt. Given the high valuation of investment grade bonds, or the narrow yield spread above government bonds, most of the returns in this asset class derive from the government bond yield element. Given we are wary of government bond exposure, the committee decided to reduce our investment grade bond holding.

The proceeds from both of these sales will be held in cash for now. This allows us to be opportunistic should we identify attractive investments in either bond markets, or other parts of the portfolio.

Alternatives and Currency

The committee made no changes to our alternatives or currency positioning.

Our alternatives exposures were analysed across four different themes.

- Risk-off exposure – these positions should benefit from an increase in market volatility, especially on the downside. This includes traditional safe haven assets.

- Absolute return strategies – these strategies aim to achieve positive returns regardless of market direction.

- Alternative credit strategies – these target alternative parts of the credit market which have a low correlation to the wider market. These can include catastrophe bonds, trade finance and convertible bonds.

- Risk-on exposure – these positions should benefit from a strong economy and rising markets but provide an uncorrelated source of return. This includes industrial commodities.

The committee are comfortable with our weighting across the four themes, given the diversification benefit they offer.

In currencies, we remain overweight in Japanese yen and Emerging Market currencies and underweight in the US dollar.

Summary of positioning

Below is a summary of our views for each asset class, from strongly negative (- -) to strongly positive (+ +).

Asset Class

| Asset class | -- | - | Neutral | + | ++ |

|---|---|---|---|---|---|

| Equities | X | ||||

| Government bonds | X | ||||

| Corporate bonds | X | ||||

| Alternatives | X | ||||

| Cash | X |

Asset Class Breakdown

| -- | - | Neutral | + | ++ | ||

|---|---|---|---|---|---|---|

| Equities | USA | X | ||||

| UK | X | |||||

| Europe | X | |||||

| Japan | X | |||||

| Asia ex-Japan | X | |||||

| Emerging markets | X | |||||

| Bonds | US Government | X | Non-US Government | X | ||

| Inflation-Linked Government | X | |||||

| Investment Grade Corporate | X | |||||

| High Yield Corporate | X | |||||

| Emerging Market Debt | X | |||||

| Alternatives | Commodities | X | ||||

| Gold & Gold Miners | X | |||||

| Property | X | |||||

| Global Macro | X | |||||

| Equity Long/Short | X | |||||

| Absolute Return | X | |||||

| Infrastructure | X | |||||

| Currency | Sterling | X | ||||

| US Dollar | X | |||||

| Euro | X | |||||

| Japanese Yen | X | |||||

| Emerging Markets | X |

Fund in focus: Morgan Stanley Investment Management – Emerging Markets Debt Opportunities Fund

What is Emerging Market Debt?

Emerging Market Debt (EMD) refers to bonds issued by governments and companies in developing or “emerging” economies. These markets typically offer higher yields, faster structural growth, and attractive diversification benefits versus developed‑market bonds.

EMD spans three main segments:

- Hard Currency Sovereign Debt – Emerging market (EM) governments borrowing in a foreign currency (e.g. US Dollars or Euros).

- Hard Currency Corporate Debt – EM companies borrowing in a foreign currency (e.g. US Dollars or Euros). A fast‑growing sector where corporates can have a higher quality rating than their own governments.

- Local Currency Debt – EM governments or corporates borrowing in their domestic currency, offering additional return potential from changes in interest‑rates and FX, which often benefit from a weaker or stable US dollar

Political volatility, currency swings and lower liquidity all play a part in increasing the risk of investing in emerging markets vs developed markets, which is why selecting a strong manager is particularly important in this allocation.

Fund objective and philosophy

The Fund buys EMD with a focus on absolute returns rather than relative benchmark positioning. Its philosophy is built on three principles:

- The universe is vast and differentiated: The team covers 100+ emerging and frontier market economies, giving them access to an extraordinarily wide investable universe

- Idea generation drives returns: Every portfolio manager, analyst, and trader is tasked with generating ideas and is accountable for the absolute performance of those ideas, reducing key person risk and gives ownership to each trader.

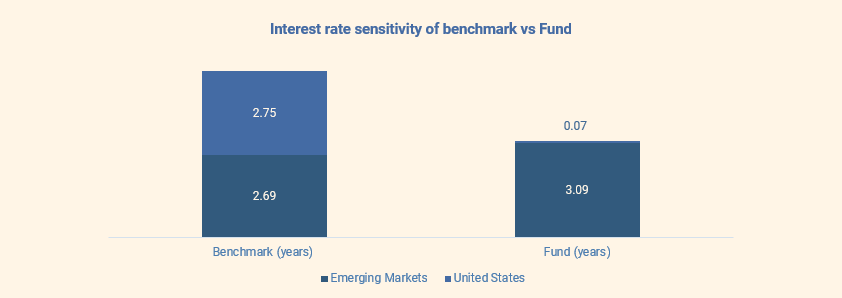

- Pure EM exposure: A noteworthy feature, the team removes the interest rate risk from hard‑currency holdings, keeping the portfolio focused on EM‑specific risk rather than global bond moves.

Investment personnel strategy

One of the biggest advantages of this strategy is the depth and stability of the team. Although the group was originally part of Eaton Vance, the acquisition by Morgan Stanley has strengthened resources and broadened global access. This team is globally distributed, conducting 60–80 country visits per year, giving them on the ground insights that generic macro data simply cannot offer.

The strategy blends deep fundamental research with bottom‑up security selection, assessing each country’s direction of change across politics, economics, and ESG momentum. Information sources include government officials, central banks, academics, think tanks, journalists, and private sector corporates providing a deliberately broad sounding board for the team to make their assessments.

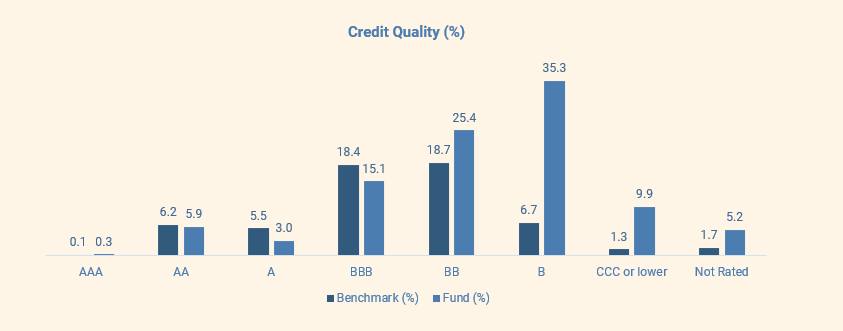

Current Positioning and Key Metrics

| Fund | Index | |

|---|---|---|

| Countries Represented | 66 | 86 |

| Off Benchmark (%) | 40.1 | - |

| Local Sovereign (%) | 54.0 | 50 |

| External Sovereign (%) | 16.6 | 25 |

| Corporate (%) | 27.8 | 25 |

| Foreign Currency Exposure (%) | 60.2 | - |

| Yield to Maturity (%) | 12.1 | 6.0 |

Source: MSINVF Emerging Markets Debt Opportunities Fund | Morgan Stanley

Saltus rationale

Specific to the MSIM EMDO fund, their preference for high yield and low interest rate risk bonds offers a compelling blend of income and diversification. We think this is particularly attractive in volatile markets as we have seen since Covid-19.

Further, the team are some of the best in class, with a genuine depth of knowledge and access across the local markets they invest in. Despite turbulent periods for global fixed income, the Fund has delivered persistent, competitive returns within its sector, supported by a disciplined risk‑management framework.

EMD more broadly provides powerful diversification in portfolios vs. developed market bonds. The exposure allows us to benefit from domestic EM growth drivers, improving fundamentals in these regions, and FX trends, in particular a weakening dollar.

Summary

The Morgan Stanley Emerging Markets Debt Opportunities Fund is a high‑conviction, actively managed strategy offering high income, broad diversification, and a disciplined approach to EM investing. For clients seeking enhanced fixed‑income returns with experienced oversight, it remains a key component of our diversified portfolios.

Asset Allocation Committee

The committee consists of several senior members of the investment team, all partners, who invest their own money alongside clients. The committee consists of:

Charles Ambler

Co-Chief Investment Officer, Saltus Asset Management Team

David Cooke

Co-Chief Investment Officer , Saltus Asset Management Team

Andy Cawker

Chairman of the board of Saltus Partners LLP and Saltus Asset Management, Saltus Asset Management Team

Joshua Biele

Investment Analyst, Saltus Asset Management Team

Tom Harrison

Investment Analyst, Saltus Asset Management Team

Clive Martin

Financial Planner, Saltus Asset Management Team