Investment conditions

Growth (economic)

The global economy is in rude health when looking at Gross Domestic Product (GDP) growth in isolation, however other growth indicators are showing signs of weakness, especially when viewed on a country-specific basis. The US continues to outshine most other countries with its economic strength, and this is expected to continue as the US Federal Reserve (The Fed) start bringing down interest rates. Fears of a ‘hard landing’ – a higher interest rate-induced economic slowdown – have receded, and we may be slowly returning to a ‘no landing’ scenario in which the economy doesn’t slowdown in any meaningful way, inflation is more stubborn, and rates have to stay higher for longer.

On the other end of the spectrum, Europe’s growth machine is stuttering, especially in the manufacturing powerhouse of Germany. Economic conditions in Germany languish in recessionary territory. Of the other major economies, the UK growth picture continues to improve, Japan remains robust, and China is on life support and requires continuous stimulus to keep going.

Inflation continues to fall on a reasonably synchronised basis. In the US, the latest release showed inflation slowing to 2.4%, this compares to Japan at 2.5%, UK at 1.7%, and Europe at 1.7%. Inflation falling towards or below target levels is giving central banks the space to reduce interest rates, with the exception of Japan which is still enjoying a comeback from its ‘lost decades’ (Japan’s Economic Renaissance | Saltus).

Unemployment numbers remain near historic lows across the board, a reflection of the tight labour supply conditions in the post-Covid economy. US jobs creation is back on the rise, but away from the headline data there are signs of softening, for example hiring rates and quitting rates are falling meaning people are less comfortable quitting their jobs, possibly because they fear a downturn or because other companies aren’t hiring. Wages are still growing at a healthy clip though, given the low levels of unemployment. With inflation coming down, this is supporting the consumer which remains a key pillar of economic growth.

Third quarter earnings have so far been positive, but there are pockets of weakness – for example, consumer companies – which could be a warning sign about a forthcoming slowdown. On the whole though corporates are still in a strong position, enjoying high margins and growing profits. Corporate spending is rising too, a signal that businesses are feeling confident in their future outlook.

Many of the above data points are lagging indicators, telling us what has happened. By looking forward at leading indicators to see what could be in store, we can generally see a positive picture. The Composite Purchasing Manager Index (PMI) is based on business survey data in both manufacturing and services, and is in expansion territory in the US, UK, Japan and China. The weak link is Europe, especially Germany.

All in all, the committee does not see any major changes in growth conditions to warrant wholesale shifts in stance.

Interest rate & liquidity environment

The Fed kicked off their rate cutting cycle with an outsized 0.5% reduction at their meeting in September. This was accompanied by commentary from Fed speakers saying they were now focusing more on the employment side of their mandate than inflation. The read from this was the Fed can see meaningful weakness in the labour market, enough to justify a larger cut. Every US data release continues to be pored over for signals over the path of interest rates from here. Given the latest strong US labour market data, the expectations for rate cuts have been scaled back. The Fed has been adamant they are data driven and so it is hard to predict what their next move will be.

Elsewhere, the gloomy data in Europe is forcing the European Central Bank into more rate cuts. The base rate is currently at 3.25% so already meaningfully lower than the US and the UK. In the UK, the Bank of England left the base rate at 5.00% at their September meeting as they want to avoid cutting too fast. Recently though Andrew Bailey, the Governor of the Bank of England, admitted they could be “a bit more aggressive” about cutting rates so we expect more to come over the coming months.

Liquidity in the financial system remains plentiful and financial conditions loose, even in the face of central bank balance sheet reductions. This is supportive of the current benign investment environment.

The committee remain of the view that we have entered a sustained rate cutting cycle now inflation looks to be under control but are aware these cuts may be slower to materialise than what is forecast.

Valuations & earnings outlook

Coming into the last quarter of 2024, analysts are still optimistic on global earnings growth and forecast 9.4% growth for 2024. The broad consensus is for strong earnings growth to continue into 2025. Emerging Markets is the area of largest expected Earnings Per Share (EPS) growth over 2024 and 2025, with the UK and Europe lagging, but still positive. Profit margins look to have rolled over in most regions.

The US is the only major region meaningfully overvalued versus its history on a 10-year average price to earnings multiple. Japan and Emerging Markets are no longer cheap but in line with long term averages. Europe and the UK are still very cheap by their historical standards, justified to some extent by their earnings outlook.

Within sectors, small companies and traditional value stocks are still cheap, but the earnings outlook for a lot of these companies is negative, which again is warranting these low valuations. This is not the case in all markets though, and we have sought exposure to UK, Japan and European smaller companies given the opportunity for active managers in these areas to outperform.

Sentiment / flows

Market sentiment is beginning to look extended. The US stock market is trading above its long term moving average, market breadth is strong meaning there is a high volume of stocks that are rising, and investors are typically not using put options to hedge their downside exposure. Market volatility is rising but still at relatively supressed levels, and stocks have been outperforming bonds. All these indicators point to positive sentiment that is at risk of becoming excessive.

A popular survey of fund managers in October registered the biggest jump in optimism since the depths of the pandemic. Allocations to stocks surged, bond exposure sank, and cash levels fell. Weekly flows into financial market assets have been strong over the last three months, above the average for 2024, based on global fund flow data.

Views by asset class

Equities

Despite tremors in equity markets at the beginning of August and September, they have continued their upward trend during the period. China has been the standout performer given the recently announced policy measures. These measures were seen as being stimulative for both financial markets and the economy, and at one point the CSI300 – an index of the largest Chinese companies – was up around 30% from its lows in mid-September. This optimism rubbed off on the Emerging Market indices too as China is both a large component and dominant in the associated regions.

In the US, the supremacy of the technology sector continues to recede, with the broader market catching up. This has benefitted our position in the equal-weighted S&P500 index, which was a way for us to avoid over-exposure to the technology sector given extended valuations. Japan and European markets also posted healthy gains, with the UK being the relative laggard.

The positive economic backdrop of strong growth, falling inflation and lower interest rates should help equity markets to consolidate their gains into year end. Looking into 2025, if expected earnings growth materialises this should support further gains. However, these expectations do not leave much room for disappointment and given stretched valuations in some corners of the market, could result in weakness if the optimism isn’t justified.

The committee’s view on equity markets hasn’t changed materially since the last meeting, and so there was little proposed change to our equity book. We want to maintain our exposure to high-quality companies whilst not being too exposed to the US technology sector. We also do not want to be too exposed in either direction to value or growth sectors, and so a broad market exposure in the US is maintained.

Regarding our Japanese equity exposure, we will continue our rotation from large companies into smaller companies on better earnings expectations and lower valuations. Please see the below the ‘Manager in Focus’ section for more detail about how we are implementing this decision.

Government bonds

For most of the period government bond markets performed well as interest rates were cut, and expectations of future cuts grew. Then at the beginning of October, we saw a stronger than expected US employment number that pushed bond yields back up (and prices down). These gyrations have meant bond volatility has increased, reflecting the uncertainty around the path of the economy and interest rates from here.

We continue to favour a position in government bonds in lower-risk portfolios given their defensive characteristics in the event of an economic slowdown. These act as a diversifier to the equity positions. Our current government bond exposure is an even blend of US and UK government bonds. These markets have the highest yields in the G7, giving us more valuation support.

Corporate bonds

Corporate bonds have continued to perform well and support client portfolios. This asset class does look expensive though, and so we continue to hold our position where it is.

Alternatives

Given the high real yields on offer in selected bond markets, and their protective characteristics, the committee has decided to incrementally move from low volatility alternatives to fixed income in lower risk band portfolios. When real yields are at these elevated levels, fixed income as an asset class has tended to outperform and has an attractive forward risk/return profile.

The committee discussed our gold and gold miners holdings in light of recent positive performance of both. Even though gold has reached all-time highs, the committee decided to leave our position unchanged given the structural tailwind of increased global central bank demand. So long as the geopolitical environment remains strained, especially between the US and China, there should be consistent underlying demand for the yellow metal. Gold miners have been performing well with the gold price, but we still think they are undervalued at current levels and so maintain a significant position here.

Summary of positioning

Below is a summary of our views for each asset class, from strongly negative (- -) to strongly positive (+ +).

Asset Class

| Asset class | -- | - | Neutral | + | ++ |

|---|---|---|---|---|---|

| Equities | X | ||||

| Government bonds | X | ||||

| Corporate bonds | X | ||||

| Alternatives | X | ||||

| Cash | X |

Asset Class Breakdown

| -- | - | Neutral | + | ++ | ||

|---|---|---|---|---|---|---|

| Equities | USA | X | ||||

| UK | X | |||||

| Europe | X | |||||

| Japan | X | |||||

| Asia ex-Japan | X | |||||

| Emerging markets | X | |||||

| Bonds | Government | X | ||||

| Index-linked | X | |||||

| Investment grade | X | |||||

| High yield | X | |||||

| Emerging market | X | |||||

| Convertibles | X | |||||

| Structured credit | X | |||||

| Alternatives | Commodities, gold + miners | X | ||||

| Macro hedge + other alts | X |

Investment Committee Q&A

In this feature we attempt to lift the lid on the process and our views by interviewing one of the decision-makers: David Cooke, Co-Chief Investment Officer

The Committee last met six weeks ago, what has happened since then?

It has been an eventful period with the major events of note being a recovery in global market sentiment and the arrival of long-anticipated interest rate cuts in the US. The 0.5% reduction in US interest rates was larger than expected and provided a boost to markets, mainly because investors could now see almost the entirety of developed economies in a co-ordinated interest rate cutting cycle. This could only have happened after the threat from runaway inflation had been (largely) tamed. A series of stronger than expected datapoints on the US economy plus a serious stimulus programme in China also combined to alleviate fears of a ‘hard economic landing’, further improving investment sentiment. This combination of factors has meant the erratic trading of the summer has started to give way to continuing gains from risk assets (equities and credit), with upward momentum strong enough to overcome external drags from the oil market, where prices have risen from recent lows to reflect the increase in geopolitical risk over the last six weeks.

What has been working well for portfolios, and what has been less effective?

Our exposures to risk assets have been the main drivers of performance. Equities in general have risen, with particularly good contributions from the Asian region (post Chinese stimulus announcements) and from our equal-weighted S&P500 index tracker fund. This position was chosen to pick up a broadening out in the leadership of the US equity market, as the largest technology companies begin to mark time after an exceptional run year to date. Commodities as mentioned above were strong in energy, copper and precious metals. Gold in particular has been a strong performer as structural long term buying by non US central banks continues to underpin prices. There were not too many notable portfolio detractors over the period, with the weaker performers spread across certain geographies (European equities) or styles – market neutral alternative strategies had a mixed month as they struggled to cope with the sharp swings in market mood.

Economic data has been mixed, do you see a clear trend about where we are headed next?

The trends are becoming clearer, with the combination of US interest rate cuts and Chinese stimulus increasing the likelihood of solid economic growth in the year ahead. The US economy in particular remains in rude health. This relatively more robust economic outlook is not without its risks though, as it may also increase the chances of inflation remaining higher than desired and hence reducing the scope for further interest rate cuts. This is a live issue, and the next few months’ data releases will be carefully reviewed. We would expect market conviction on underlying trends to increase as we move through the next few months, with our own view remaining that the outlook is more ‘glass half full’ (i.e. both inflation and growth trends will end up supportive of ongoing investment gains).

Do you see the periods of volatility like we saw in early August and early September becoming more frequent?

Unfortunately, yes, as these periods of volatility are a function of powerful underlying trends that aren’t going away any time soon. There is major event risk surrounding the outcome of the US elections, at a point when the geopolitical atmosphere is also febrile. The financial system, particularly in the government sector, is heavily indebted and therefore prone to sharp shifts in market mood. This mood is often driven by short term data, which can be hard to predict in advance, leaving plenty of scope for surprises. The best way to navigate an environment such as this is to be as broadly diversified as possible across assets, styles and geographies, as each will have idiosyncratic drivers that help insulate portfolios from this heightened volatility which is now a fact of life.

Given the recent policy announcements in China, and the performance of the stock market in response, are you considering an allocation there?

We have allocations to investments which will benefit from the Chinese economy recovering – such as Asian equities or copper, but we are not considering allocating to China directly. Hurdles to investing (the risk of government interference in capital markets) remain too high. If these issues are addressed, then we will consider a direct allocation.

The European economy seems to be slowing down at a faster rate than others, what is your view on European equity markets in light of this?

Our view is that there is not a strong investment case for having a large exposure through the traditional ‘buy and hold’ strategies. We would prefer to have our exposure in an active long/short manager, which is better suited to an environment where there is a wide dispersion in performance across sectors and geographies. Small exposures might be suitable in the smaller company arena given the attractive valuations but that is also a case that could be made for the UK market, where we would prefer to put incremental capital to work.

Gold keeps hitting record highs, what is the view from here for your gold holdings?

We continue to believe that gold will do well and thus we will be keeping our exposure to bullion and, where appropriate, gold mining shares. There are multiple drivers for the gold price, with the ‘new’ structural demand from central banks seeking to diversify away from dollar reserves (which can be confiscated by the US) remaining a powerful driver to the upside. Gold is also now attracting inflows from financial investors as they seek some insurance against the long run issues surrounding government balance sheets, which act to undermine fiat currencies. The combination is creating powerful momentum which we do not see abating in the near term.

Manager in focus: Nomura Japan Small Cap Equity Fund

Summary

The Nomura Japan Small Cap Equity Fund is a long-only equity fund, in which bottom-up, stock-specific analysis is used to find companies that are significantly undervalued relative to their growth prospects.

As the name suggests, the fund focuses on finding opportunities in small companies that are listed on the Japanese stock market. These companies can range from $100m to $7bn in size and are spread across a range of industries and sectors.

The team is one of the largest in the Japan small cap space and are based in Tokyo. They make a point to meet their investee companies in person, as there is typically little publicly available information. There is a larger opportunity in this part of the market to identify mispriced stocks given this lack of publicly available information, compared to investing in larger companies which tend to be more well covered.

Nomura and the team

Nomura is one of the largest and most renowned financial institutions in Japan, and indeed globally. Nomura Asset Management has been actively managing Japanese equity portfolios since 1959, and Japanese equities make up half of its $570bn of AUM. They are considered specialists in the region and have deep roots in Japanese capital markets and industry.

They have a substantial research team. Makoto Ito is the lead portfolio manager. He joined Nomura in 2008 as an equity analyst and has been running the fund since 2015. He is supported by five other portfolio managers, and 21 analysts. This gives the fund the ability to cover a wide universe of opportunities.

Investment philosophy and process

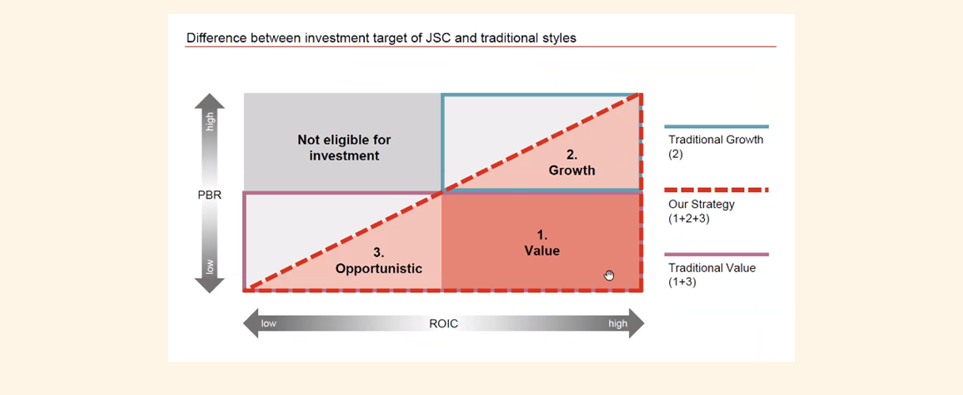

The team aims to find companies where their estimation of intrinsic value differs significantly from the current market valuation, using a price-to-book value multiple. This does not necessarily mean the multiple is low, in fact the price-to-book multiple of their holdings is typically higher than average, as they look for companies with solid growth prospects. They also aim to identify companies with catalysts for valuation improvements.

The fund holds a mix between ‘value’ stocks, ‘growth’ stocks and ‘special situations’ stocks, which gives it diversification benefits as performance is not dependent on any one factor. The composition between these factors changes over time. At present, there is a slight value bias.

Performance

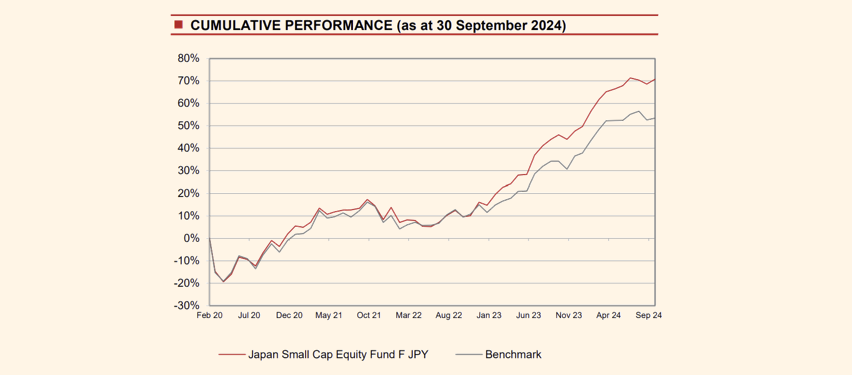

Since the inception of the European version of the Nomura Japan Small Cap Equity fund in February 2020, it has returned 12.2% on an annualised basis. This compares to the benchmark (Russell/Nomura Small Cap Index) at 9.7%.

Saltus investment case

There are a number of reasons why we have been increasing our exposure to the Japan small cap space. We have been funding this increase from our large cap fund. We believe Japan’s economy is on the cusp of a structural recovery, as evidenced by rising real wages, steadily rising inflation, and normalising monetary policy. If this momentum is sustained, smaller companies are well positioned to benefit as they are more sensitive to domestic economic conditions given the bulk of their revenues and profits are generated at home.

Given this domestic focus, smaller companies are less exposed to currency fluctuations. Over the last year or so, smaller companies have underperformed larger companies as a weaker Japanese yen has benefitted exporting companies, as their exports have become more competitive globally. As the Bank of Japan now has a tightening bias, compared to loosening by other major central banks, the Japanese yen is starting to strengthen. Should this continue, small companies should outperform especially if the Japanese economy maintains its momentum.

Another factor behind this allocation is the ongoing corporate reform in Japan (again more detail on this can be found in our recent article Japan’s Economic Renaissance | Saltus). Smaller companies have more to gain from these reforms. There is more scope for capital efficiency, starting valuations tend to be lower, and there are more takeover targets in this part of the market. In fact, the fund looks for companies that could be takeover targets as a driver of outperformance.

This is a notable example of the two-stream Saltus investment process. From an asset allocation perspective, we wanted to increase our exposure to this asset class due to many of the reasons mentioned above. Then we have selected the fund which we think gives us the best exposure to the theme. The positive results can be seen in both recent outperformance of small caps relative to large caps, and also this fund relative to the benchmark.

Saltus use this fund as part of a diversified portfolio. This is not a recommendation to invest in this fund. Saltus will not be liable for any losses incurred as a result of investing in this fund.

Asset Allocation Committee

The committee consists of several senior members of the investment team, all partners, who invest their own money alongside clients. The committee is led by:

Charles Ambler

Co-Chief Investment Officer, Saltus Asset Management Team

David Cooke

Co-Chief Investment Officer , Saltus Asset Management Team